Key takeaways

- The Low-Income Country Debt Sustainability Framework (LIC-DSF) is the primary “early warning system” used by the International Monetary Fund (IMF) and World Bank to manage borrowing for 70% of low-income countries.

- A country’s risk rating directly dictates whether they receive funding as concessional loans or as debt-free grants.

- The framework’s original 2006 design fails to be appropriate for today’s diverse creditor base, including the significant increase in domestic borrowing and private external debt.

The LIC-DSF is the primary analytical tool used to assess debt sustainability in low-income countries. Jointly developed by the World Bank and the IMF in 2006 and updated periodically since, it is designed for countries with limited access to international capital markets. It aims to function as an early warning system, identifying when debt dynamics are becoming inconsistent with sustainable repayment capacity and signalling the need for corrective action.

Debt vulnerabilities have intensified following successive global shocks, including the COVID-19 pandemic, and a rise in interest rates by major central banks. Countries operating under the LIC-DSF, such as Zambia, Ethiopia, Ghana, and Suriname, have undergone complex and protracted restructurings, exposing strains in the international debt architecture and the limits in the uptake of early risk signals. Far from isolated cases, many others — particularly in Africa — are facing mounting repayment pressures.

This is about more than financial stability. These countries must reduce poverty and inequality while financing the transition to more sustainable and resilient economies. The central questions are whether current debt levels are compatible with these objectives; how to address obligations that are either unfinanceable, unaffordable, or unsustainable, or constrain essential investment; and how to mobilize adequate and affordable financing, drawing lessons from past experience.

At the same time, many of these countries face growing pressure to mobilize domestic resources in a context of declining official development assistance (ODA) and repeated global shocks. This raises important questions about how debt sustainability assessments relate to domestic revenue capacity, fiscal space, and external stability.

Revising the LIC-DSF is therefore essential not only to prevent a broader debt crisis, but also a development crisis.

What is the LIC-DSF, and who is it for?

The LIC-DSF is a forward-looking risk assessment tool. Like any debt sustainability analysis (DSA), it projects debt-burden and debt-service indicators over the medium term, compares them against predefined thresholds, and assigns a risk rating of debt distress. These ratings are intended to guide borrowing decisions by multilaterals, inform prudent debt management, and anchor restructuring negotiations, when needed.

The LIC-DSF was adopted following the large-scale debt relief initiatives of the late 1990s and early 2000s. While the Heavily Indebted Poor Countries Initiative and the Multilateral Debt Relief Initiative focused on reducing inherited debt stocks, the LIC-DSF aimed to prevent a renewed buildup of unsustainable debt by making concessional lending dependent on a standardized analytical framework.

The framework applies to the world’s most vulnerable economies, accounting for 70% of the world’s poor. The IMF identifies these countries through its Poverty Reduction and Growth Trust eligibility framework based on income level and market access. The list of countries almost entirely overlaps with those eligible for the World Bank’s concessional lending arm, the International Development Association (IDA).

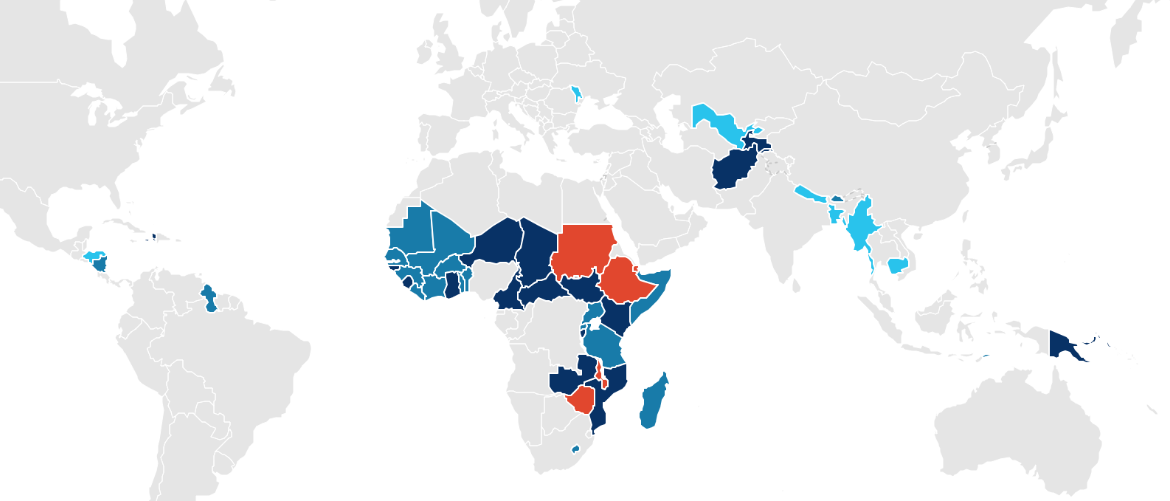

Countries applying the LIC-DSF framework and their level of debt distress according to the framework

How is the framework used in practice?

The LIC-DSF performs three main functions in practice: it signals when borrowing and lending become risky, shapes the terms on which multilateral financing is granted, and provides an analytical benchmark in situations of debt distress.

- First, the framework operates as a forward-looking risk assessment tool for debt managers in countries where it applies. By projecting debt-burden and debt-service indicators and comparing them to policy-dependent thresholds, it assigns a rating of low, moderate, or high risk of debt distress. These ratings are intended to signal when debt dynamics are becoming inconsistent with sustainable repayment capacity, encouraging debt managers to respond preemptively before vulnerabilities become acute.

- Second, the LIC-DSF is embedded directly in the operational rules of multilateral financing, particularly in the World Bank’s International Development Association. LIC-DSF risk ratings determine the mix of grants and credits that countries receive: low-risk countries receive standard concessional credits, moderate-risk countries receive a mix of credits and grants, and countries at high risk—or already in distress—receive their allocation entirely in grants. Through this mechanism, the framework links assessments of external debt vulnerabilities to the terms of concessional financing and aims to discourage excessive accumulation of non-concessional debt.

- Finally, the LIC-DSF provides a reference point in debt restructuring processes. In cases of distress, the framework helps anchor discussions about the scale of adjustment required to restore sustainability and provides a common analytical basis for negotiations among debtor governments, multilateral institutions, and other creditors.

Together, these functions make the LIC-DSF more than a technical diagnostic: it operates as a coordinating device shaping expectations and decisions across the international development finance system.

Why is it under review now?

When the LIC-DSF was introduced, it was built around assumptions that reflected the financing landscape of the early 2000s. These assumptions shaped core features of the framework, such as its initial focus on public and publicly guaranteed external debt, the use of present value measures to capture concessionality, and policy-dependent thresholds of debt burden and services to GDP and exports, based on the World Bank’s Country Policy and Institutional Assessment index, including other macroeconomic indicators in later revisions.

While the LIC-DSF has been revised periodically since its introduction in 2006, reflecting evolving financing conditions and analytical improvements, the framework’s underlying structure has largely remained anchored in these original design choices, raising questions as to whether this structure still adequately captures today’s debt vulnerabilities. The current review is particularly significant due to the scale of the shift in the debt landscape since the framework’s original design.

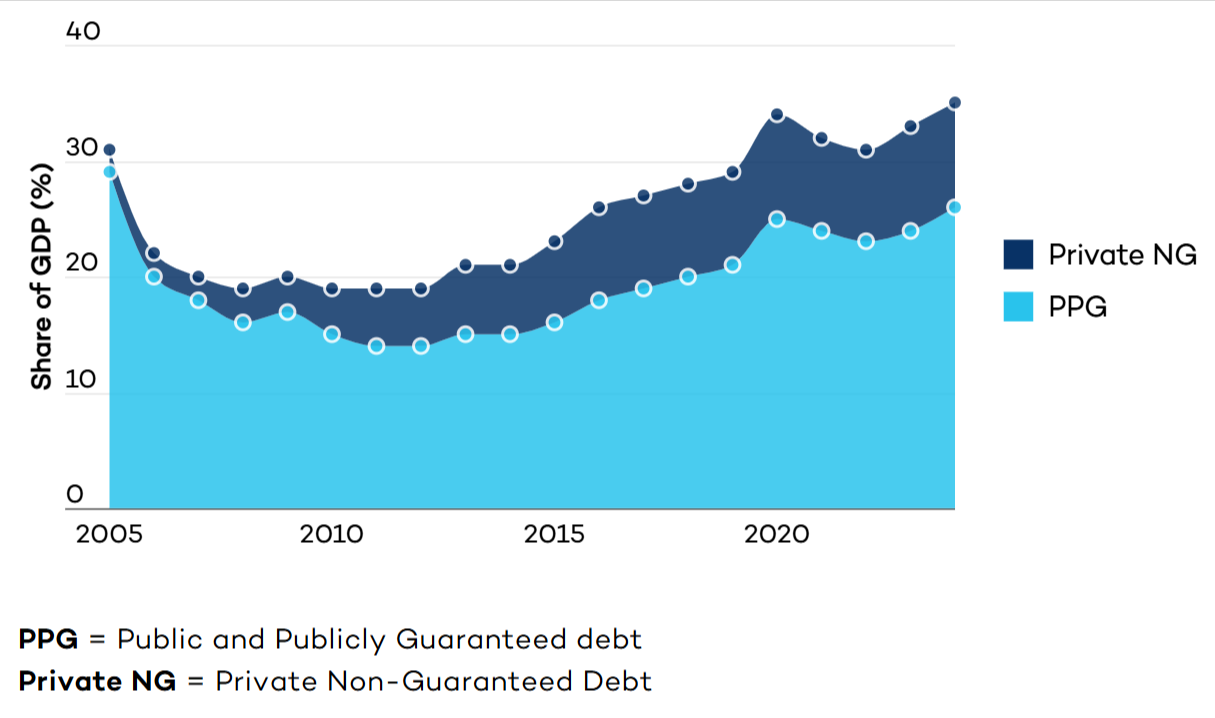

One important shift concerns the composition of debt. At the time the LIC-DSF was introduced, most low-income countries relied predominantly on concessional financing from multilateral institutions and Paris Club creditors. Today, their creditor base is far more diverse. Domestic borrowing — in local currency and held by residents — has increased significantly. At the same time, private external debt that is not publicly guaranteed has also grown, expanding the stock of liabilities that may generate external repayment pressures but that are not always fully captured in traditional assessments focused on public debt.

Long-term external debt to GDP for IDA-eligible countries

External vulnerabilities have also become more salient. Many low-income countries face tighter external financing conditions, rising external debt-service obligations, and growing pressures on foreign exchange earnings. These dynamics have become particularly visible following a series of global shocks — including the COVID-19 pandemic, the war in Ukraine, the sharp tightening of global financial conditions, and, more recently, escalating geopolitical fragmentation affecting trade, energy, and capital flows.

External vulnerabilities have also become more salient. Many low-income countries face tighter external financing conditions, rising external debt-service obligations, and growing pressures on foreign exchange earnings. These dynamics have become particularly visible following a series of global shocks — including the COVID-19 pandemic, the war in Ukraine, the sharp tightening of global financial conditions, and, more recently, escalating geopolitical fragmentation affecting trade, energy, and capital flows.

WB-IMF LIC-DSF risk assessment by country

Taken together, these developments have prompted questions about whether the LIC-DSF’s traditional indicators — originally designed for a different debt structure — fully capture the evolving sources of risk faced by low-income countries, and whether they provide sufficiently timely signals when debt dynamics are becoming increasingly difficult to sustain.

What are some of the key critiques of the framework?

Most critiques of the LIC-DSF have focused on its methodological and conceptual features. A growing literature highlights several limitations in the framework’s analytical design. First, analysts point to its limited integration of public investment needs, particularly spending related to climate adaptation, resilience, and broader development objectives. This has raised concerns that the framework may not adequately capture the trade-offs between debt sustainability and development financing.

Second, critics identify an optimism bias in macroeconomic projections, arguing that baseline scenarios may rely on overly favourable growth or fiscal assumptions, which can delay the recognition of debt distress. Third, scholars have questioned the discretion involved in assigning final risk ratings, noting that the use of judgment beyond model-based indicators can reduce transparency and weaken the consistency between analytical outputs and policy conclusions. Civil society organizations have echoed these concerns, calling for a more transparent and development-oriented framework that better reflects countries’ social and climate priorities.

While these critiques have provided important insights, they have largely remained at the level of methodological refinement. What has been largely missing from the debate is an assessment of how the LIC-DSF functions in practice. The framework is not only an analytical tool; it is used to guide debt management decisions, inform multilateral lending policies, and shape the dynamics of debt restructuring negotiations. Reform proposals should therefore consider not only the framework’s methodological design but also the practical uses and incentives it generates in real-world policy processes. These issues will be discussed further in an upcoming report.

Related Articles

Here is a list of articles selected by our Editorial Board that have gained significant interest from the public:

What’s currently on the table, and which issues should be central to the review?

The ongoing review of the LIC-DSF has so far focused largely on technical refinements, including adjustments to macroeconomic assumptions, stress tests, and the treatment of investment and climate-related spending. While these discussions are important, they risk overlooking a structural issue in how debt vulnerabilities are assessed and how the framework is used in practice.

There are three issues that should be central to the review.

- First, there must be stronger recognition that external vulnerabilities are often a primary driver of debt distress in low-income countries. Debt crises frequently emerge not only from fiscal imbalances but also from pressures on the external account—such as terms-of-trade shocks, capital flow reversals, or foreign exchange constraints. In its current form, the LIC-DSF does not sufficiently capture these dynamics.

- Second, this requires a clearer analytical separation between fiscal and external sources of vulnerability. We therefore see merit in moving toward two complementary instruments: (i) a public DSA focused on risks emerging from the fiscal side, and (ii) an external DSA that systematically assesses vulnerabilities related to the balance of payments, foreign currency exposure, and external financing conditions. This distinction would allow for a more accurate diagnosis of the nature of debt risks.

- Third, multilateral lending decisions should place greater weight on the external sustainability assessment. In practice, lending frameworks remain heavily anchored in public debt indicators, even when external constraints are the binding source of vulnerability.

A meaningful review of the LIC-DSF should, therefore, move beyond incremental methodological adjustments and strengthen the framework’s ability to diagnose and respond to external sources of debt vulnerability.

** **

This article was originally published by the International Institute for Sustainable Development (IISD) and is republished here as part of an editorial collaboration with the IISD. It was authored by Anahí Wiedenbrüg and Fernando Morra.

Editor’s Note: The opinions expressed here by the authors are their own, not those of Impakter.com — In the Cover Photo: V&A Waterfront, Cape Town, South Africa, October 2025. Cover Photo Credit: Adedayo Adekunle