In late July 2000, six of Europe’s largest telecommunications companies gathered to bid for something they couldn’t see, touch, or immediately use. It was the right to transmit data through specific radio frequencies across Germany: mobile internet. After more than two weeks of competitive bidding, they drove the price to €50.8 billion — only for a potential edge in the future of communications.

The executives in those rooms, however, weren’t irrational. Each was making a perfectly understandable business decision. The mobile internet was the future; whoever controlled the infrastructure would control the market, and this control set aside the financial aspect. Deutsche Telekom bid because Vodafone was bidding. Vodafone bid because Deutsche Telekom was bidding. The auction’s structure meant there was no ceiling on how high the price could go — only the logic that losing was worse than overpaying.

The technology worked. 3G mobile internet eventually transformed communications. It’s impossible to imagine our world without it. The financial engineering around it, however, made no sense. European telecoms collectively took on hundreds of billions in debt to fund their buildout.

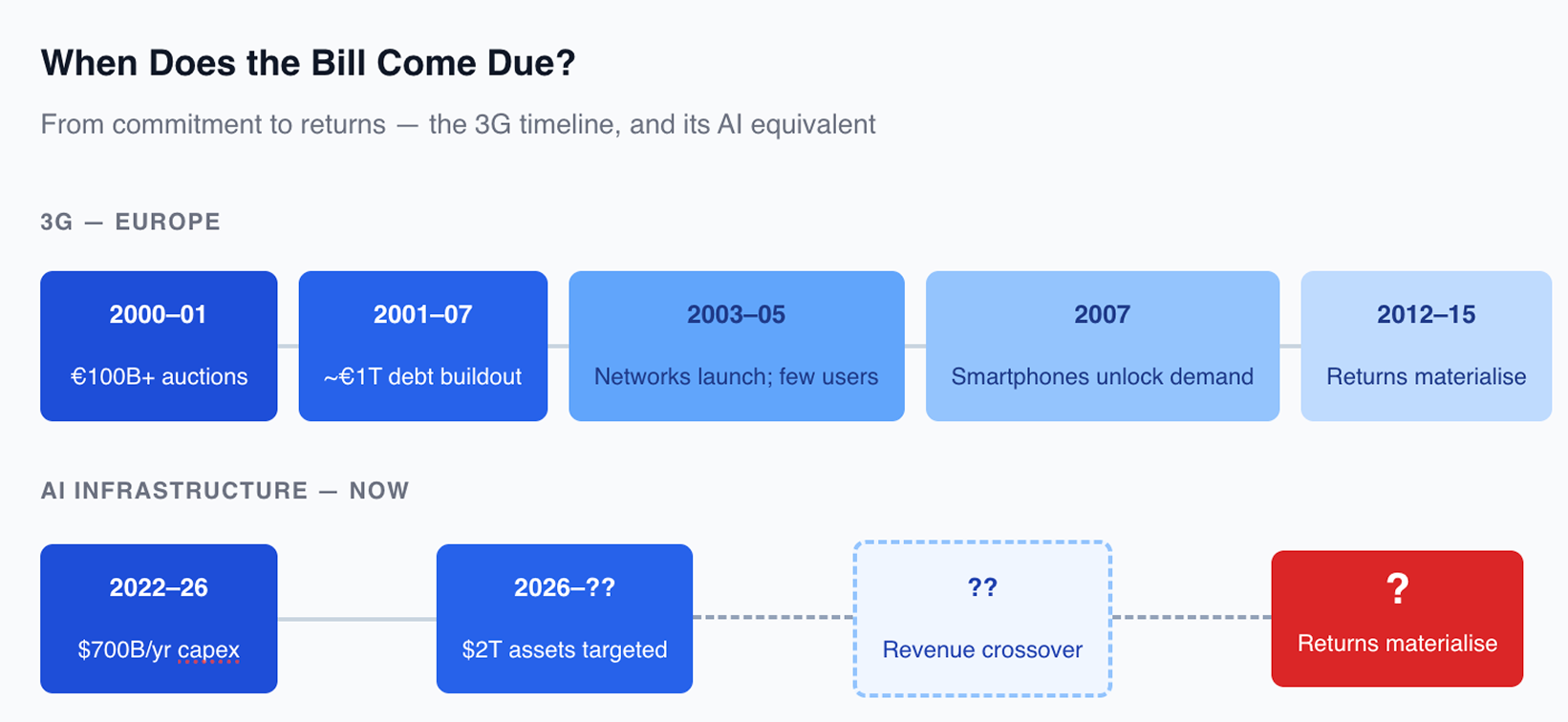

Deutsche Telekom’s share price fell more than 80% between its 2000 peak and 2002 low. European 3G networks began launching in 2003 — Hutchison’s Three network went live in the UK that March, with others following by 2005 — but into a market with almost no suitable handsets and no killer applications. It wasn’t until smartphones arrived in 2007 that meaningful consumer demand emerged. Meaningful returns didn’t materialize until around 2012, more than a decade after the auction rooms closed.

The technology worked. The timeline did not.

Hints at the AI bubble

In 2025, the world’s four largest technology companies — Amazon, Google, Meta, and Microsoft — spent a combined $443 billion on artificial intelligence infrastructure, including data centers, specialized computer chips, and power systems. In 2026, they plan to spend roughly $700 billion.

Amazon alone has committed $200 billion for the year — a near 50% jump from 2025. Google is doubling its capital expenditure to between $175 and $185 billion, a figure that would push it into negative free cash flow territory. Analysts at Barclays project Meta’s free cash flow falling by nearly 90% in 2026.

The Scissors Open

Hyperscaler capital expenditure, free cash flow, and debt issuance — the gap that defines the bet

|

Combined Capex (Big 4)

↑ 58%

$443B (2025) → ~$700B (2026)

Amazon alone: $200B in 2026

|

Amazon Free Cash Flow

↓ 66%

~$33B (2024) → $11.2B (2025)

Projected negative in 2026

|

New Debt Issued (2025)

$121B

vs. ~$28B/yr historical avg

4× the historical norm

|

Sources: CNBC, Mellon Investments, 247 Wall St.

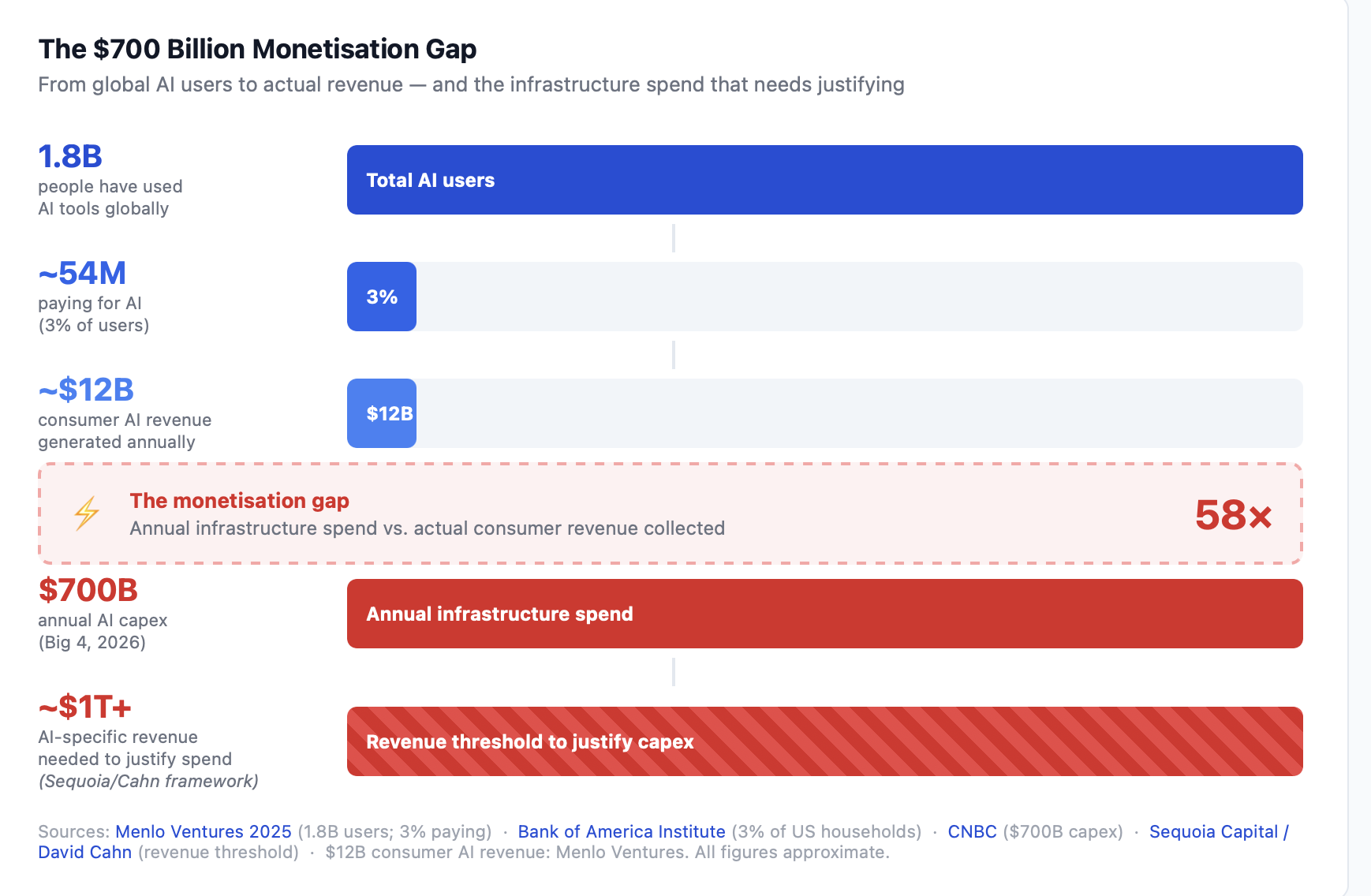

Most people won’t feel any of this directly, at least not yet. The AI tools most of us actually use are still free or cheap. The infrastructure powering them, however, is being built at a pace that is already changing the global electricity grid. For example, in Frankfurt, data centers now account for up to 40% of the city’s total electricity demand. In the United States, utility companies are making billion-dollar commitments to power plants and grid infrastructure on the assumption that AI demand will keep growing — and if it doesn’t, those costs are likely to be passed on to ordinary electricity customers.

Meanwhile, the same companies spending hundreds of billions on data centers have simultaneously led recent rounds of tech-sector job cuts — different line items, same balance sheet. When the infrastructure bet eventually needs to generate returns, the most direct route is to convert the free tiers of every AI product you use into subscriptions. But according to Bank of America Institute analysis of nearly 70 million consumer accounts, only around 3% of US households currently pay for AI subscriptions. While this figure has grown 38% year-on-year, it still represents only a small fraction of what the investment would require to be justified.

These are not struggling companies. Amazon, Google, Meta, and Microsoft collectively hold over $420 billion in cash and equivalents. Their underlying businesses — advertising, cloud computing, e-commerce — are highly profitable, which is why the companies can afford AI investments. The mechanism driving their spending is the same one that drove Deutsche Telekom into that German auction room in the summer of 2000: fierce competition to achieve the edge. This edge is the Artificial General Intelligence, the kind of AI that matches or surpasses human intelligence across most cognitive tasks.

In a 2024 analysis that has since become the benchmark reference point for this debate, Sequoia Capital’s David Cahn put the problem plainly: at then-current infrastructure spending rates, AI companies needed to generate roughly $600 billion in annual AI-specific revenue to justify the investment. The actual revenue these companies achieved from the technology at the time was around $100 billion. The gap has since narrowed, with, for example, OpenAI crossing $25 billion in annualised revenue as of February 2026. Cloud platforms are growing at rates that would be remarkable in almost any other context, but the spending has accelerated even faster. Cahn’s $600 billion threshold now looks conservative.

The question is whether $700 billion in annual capital expenditure can be justified by a technology whose revenue is still a fraction of its bill — and whether the companies writing those cheques have paused long enough to seriously consider it. In 2000, they hadn’t paused.

Related Articles

Here is a list of articles selected by our Editorial Board that have gained significant interest from the public:

A race without quitters inflates the AI bubble, as basic principles of business become irrelevant

The 3G bubble is the right historical lens for AI infrastructure — not the dot-com crash, which was primarily a story of businesses with no revenue model. 3G was a story about real technology bringing real progress for society. The only problem was financial, due to the fierce competition for the newly formed industry.

In 3G, control was not optional. You either held a license or you gave out the mobile internet market to whoever did. The price became irrelevant against the cost of losing. Today, GPUs and data center capacity function identically. No major technology company can credibly offer AI products without its own infrastructure. Capital intensity has surged to 45–57% of revenue for individual hyperscalers — ratios more typical of utilities and industrial companies than of software businesses. The infrastructure is the entry ticket.

In the 3G auction, Deutsche Telekom almost certainly realized the price for the license was too high. It bid anyway, because Vodafone was bidding. Each move forced a response.

It was a chess match, where pawns moved forward to the end of a never-ending board.

AI capex escalation follows the same dynamic, without even needing an auction room. Amazon allocated $200 billion in capex for 2026. Google responded with up to $185 billion. Meta followed. At Alphabet, analysts described the planned capex ratio — approaching 50% of revenue — as “an unheard-of level for any normal company at any point in time.” The spending is not driven by a single financial model showing positive returns. That is not the point. Market share is.

Licenses were signed in 2000. European 3G networks launched from 2003 but lacked applications. Meaningful consumer adoption came with the smartphone era from 2007. A meaningful return on investment arrived around 2012, after a decade had elapsed between the commitment and the payoff. The debt compounded, and investors waited.

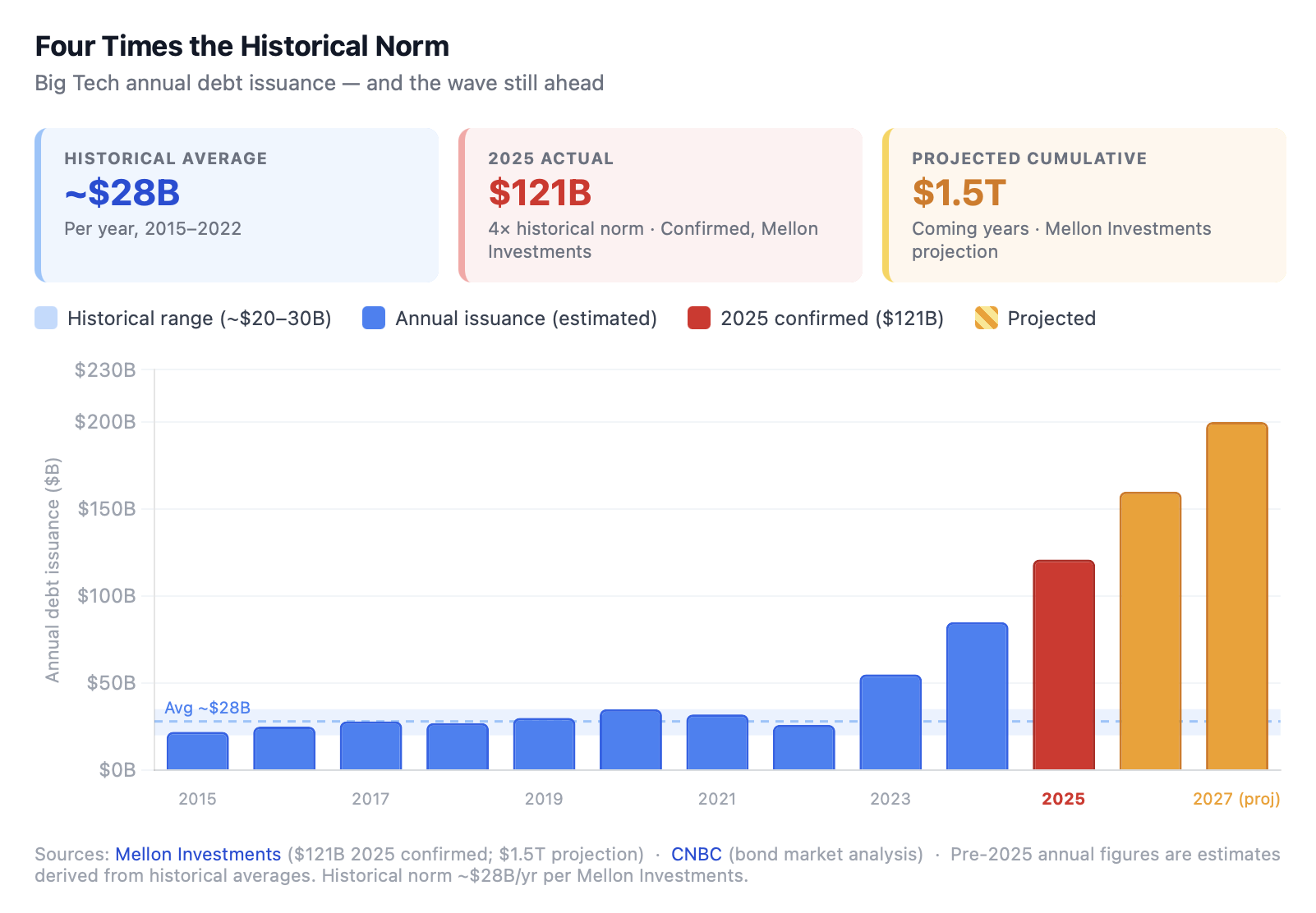

AI’s equivalent gap is currently unknown. Next-generation infrastructure will take years to deploy, more years to be adopted at enterprise scale, and more years again before the resulting revenue justifies the construction cost. No credible public projection has defined that timeline with any precision. Projections suggest $1.5 trillion in new debt issuance from the technology sector over the coming years to bridge the gap.

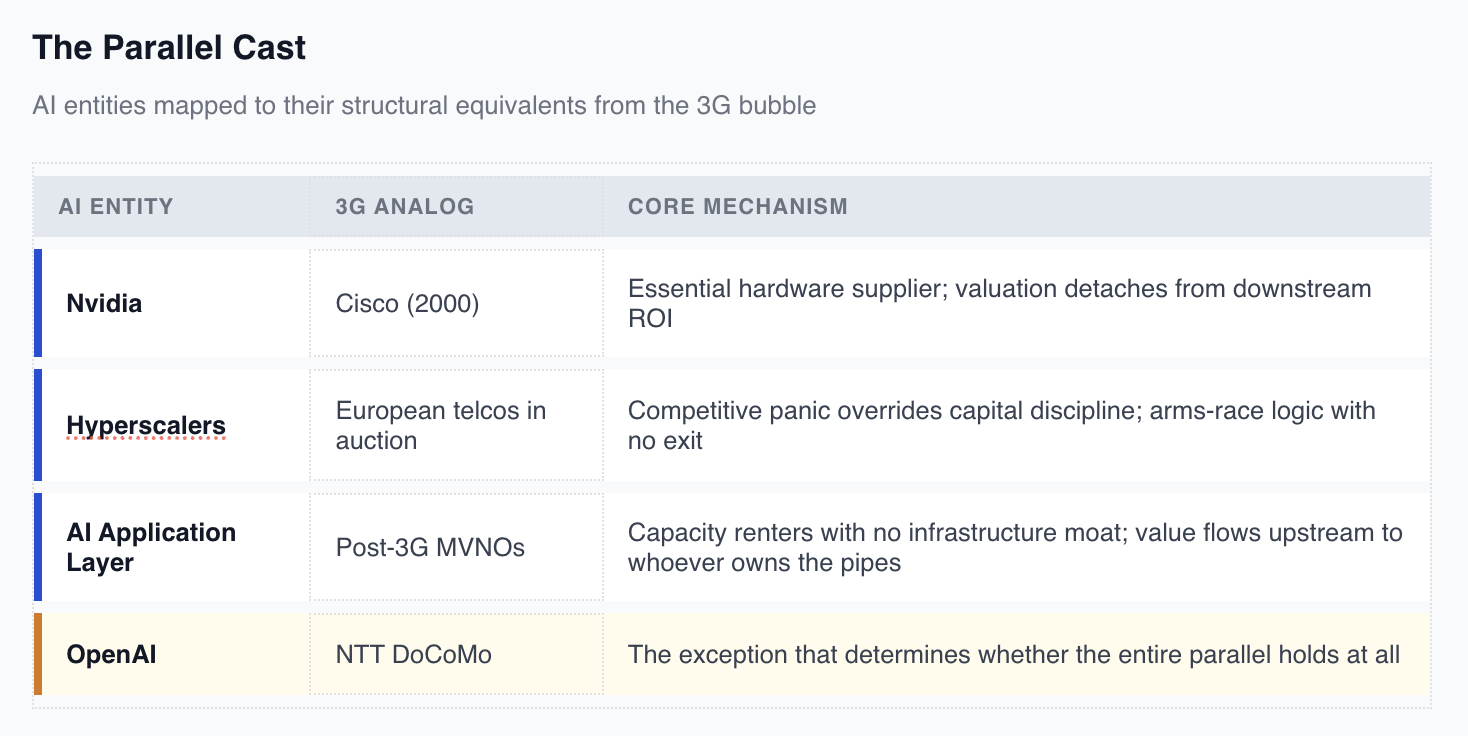

The multifaceted players in the AI Bubble

The 3G parallel maps four structural pairings with the AI ecosystem, each revealing a different dimension of how infrastructure bubbles distribute risk.

Picks and shovels business

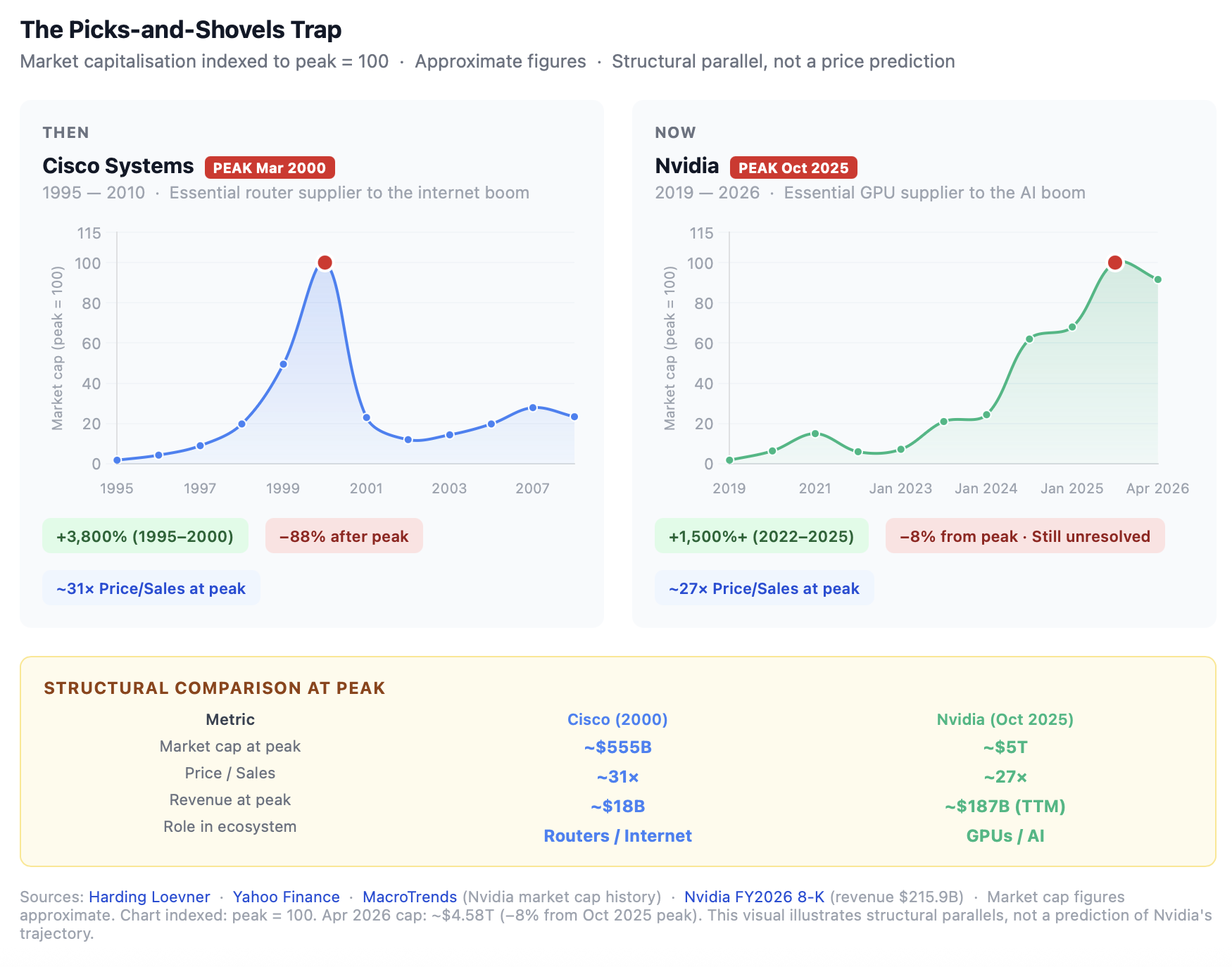

Cisco Systems was the infrastructure winner of the late 1990s Internet boom. Every network needs routers. Every router came from Cisco. Its stock rose roughly 3,800% between January 1995 and its March 2000 peak, then fell more than 85% when the bubble burst — not because its products stopped working. Customers had overbought, demand collapsed faster than anyone had modeled, while Cisco’s valuations proved too optimistic.

NVIDIA occupies the same structural position in the AI market. Its chips are essential for training large language models. Every company building an AI infrastructure needs them. NVIDIA’s market capitalization briefly exceeded $3 trillion in 2024, now it exceeds 4.5; driven by data center revenue growing at rates that would have seemed fictional five years ago. The picks-and-shovels business is excellent right up until the moment the spending slows. At this point, the demand reverses, and they discover they have more shovels than they can use. NVIDIA has diversified further into automotive, scientific, and industrial computing. Cisco never managed to diversify, which makes Nvidia more resilient. That, however, doesn’t change its structural position in this story.

Hyperscalers, or simply put, the Big Tech

BT, Deutsche Telekom, France Télécom, Vodafone — they were profitable, well-managed incumbents with real businesses. They walked into the 3G auctions and collectively committed to debt loads that took some of them a decade to repair, not because they were reckless, but because the auction structure made rational restraint collectively impossible. No single company could stop without handing the market to whoever kept bidding.

The Big Four hyperscalers will allocate roughly 75% of their investments to AI infrastructure rather than traditional cloud. To bridge the gap between capex and cash generation, debt has grown to around four times the historical annual average. Investors who previously treated hyperscaler bonds as near-riskless are beginning to demand protection: Oracle’s 5-year credit default swap rate has more than tripled since September 2025. Investors say this shift now exposes speculative AI to historically stable debt markets.

The key difference from 2000 is, again, diversification. The tech corporations are not heading for insolvency. What they face is an unsustainable period of capital with little to show for it.

AI applications and mobile virtual network operators

After the launch of 3G networks, a new category of businesses emerged: Mobile Virtual Network Operators (MVNOs) — companies that sold mobile services without owning any infrastructure. Renting capacity wholesale from networks that had infrastructure, adding branding, and selling monthly plans became a competitive business model. Most eventually went out of business when larger companies squeezed margins. The infrastructure owners extracted the value. The renters passed it along.

The AI application layer is structurally identical. It includes companies building products on top of, for example, OpenAI’s API, hence paying for access to infrastructure they don’t own. It differentiates these products at a layer where the provider could theoretically disrupt the business at any time. Enterprise demand has shown high sensitivity to price-per-token, with minimal demonstrated stickiness. Chinese and open-source models are approaching 25% market share, further eroding pricing power. The MVNO model occasionally produced winners — companies that found a genuine niche and built customer relationships that outlasted the commoditization wave. But the distribution of outcomes was brutal. The AI applications follow the same pattern as of right now.

The mastodons of the industries

BT and Vodafone won early 3G licenses across multiple markets. First-mover advantage in infrastructure was supposed to be durable — like having a patent before generics enter the market. It wasn’t; there was no set time period. New entrants didn’t wait for licenses to expire. They entered as a Mobile Virtual Network Operator (MVNO), without owning infrastructure. Competition unfolded at a service layer, pricing compressed, and the competition invalidated the premium paid for early spectrum.

The foundation model layer — OpenAI, Anthropic, Google DeepMind — paid a premium equivalent to the training costs. Training frontier models can now cost between $100 million and $500 million each. Techniques become more efficient, talent moves, and open-source models rapidly converge on comparable performance at a fraction of the cost. The first-mover premium is being competed away in the same way.

The parallel holds on how companies entered markets. It breaks on failures. In 3G, license holders retained control of the asset they paid for. The problem was failing to monetise in time, leading to crushing debt and delayed demand. In AI, the risk is not delayed demand but the acceleration of a part of the product. A regular customer focuses on LLMs, while new companies are focusing on this single aspect in their development.

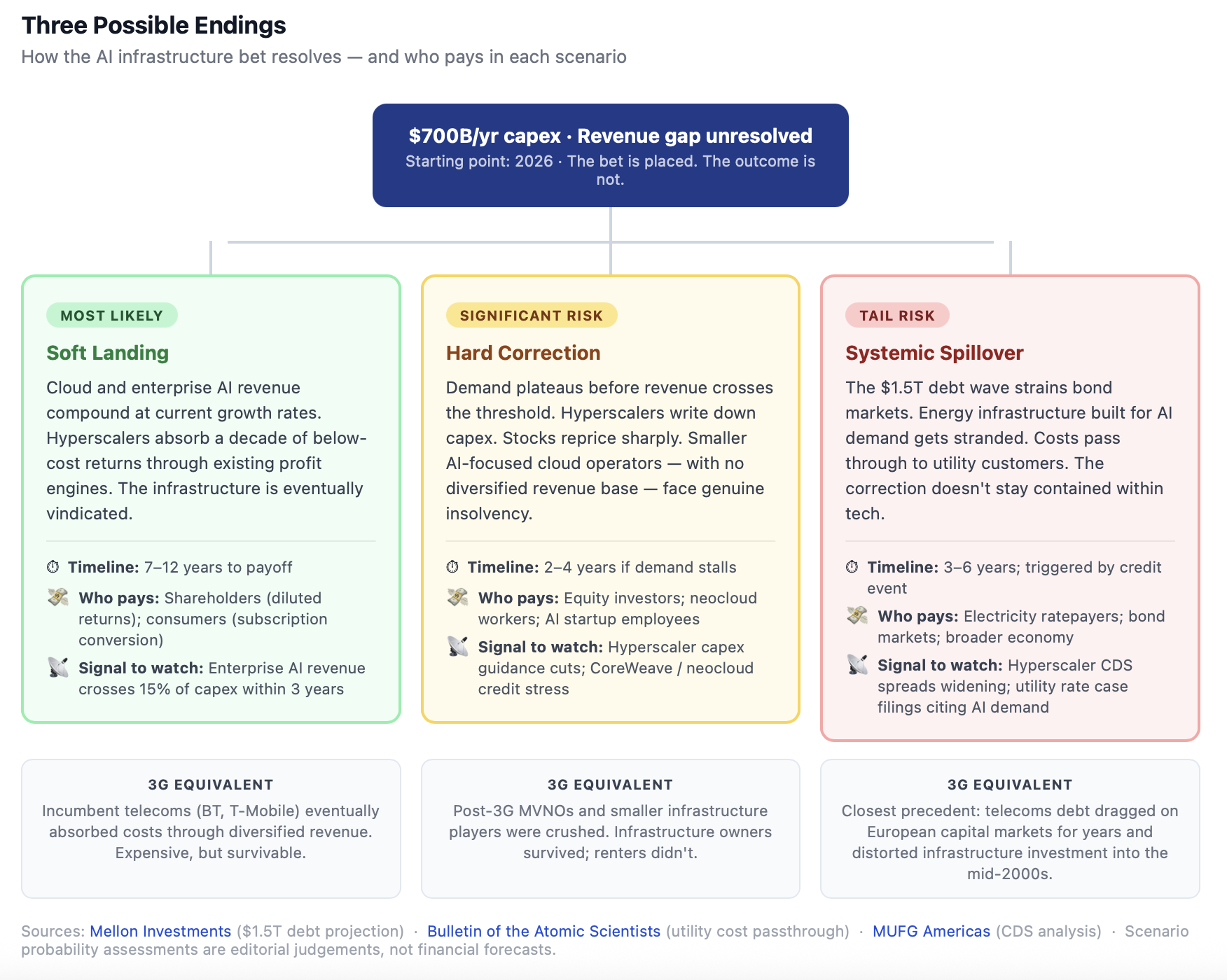

Where does the potential AI bubble differ from the 3G crisis?

The 3G analogy makes the financial future of AI more powerful, understandable, and relatable. However, it’s neither the same sector nor is the analogy perfect. The main difference is revenue and the companies’ success in developing new technologies beyond their core.

European telecoms in 2000 were financing infrastructure with debt against thin revenues. Hyperscalers’ liabilities-to-assets ratio sits at 48% — well below the S&P 500 average of nearly 80%. They hold over $420 billion in cash. Their existing businesses are enormously profitable. The risk is not the collapse of the companies building AI.

The problem lies in a decade or more of capital deployed at negative returns. The $600 billion gap Sequoia identified in 2024 has already started to close. Cloud infrastructure spending grew 25% year-on-year in Q3 2025. Google Cloud revenue rose 48% year-on-year in Q4 2025. The question is whether this trajectory can outpace a capex commitment that is accelerating in turn, not whether revenue exists.

The most likely outcome if current growth trajectories hold is that cloud growth and enterprise adoption collectively close the gap over a decade, and hyperscalers absorb the period of below-cost returns through existing profit engines. Expensive, but manageable, and eventually justified.

The demand can also plateau before revenue catches up. In that case, capex becomes unjustified, stocks drop, and smaller AI-focused cloud operators with no diversified revenue base to absorb losses face genuine insolvency. This outcome is the MVNO outcome applied to the infrastructure layer.

Lastly, as the $1.5 trillion debt wave strains bond markets, energy infrastructure built around AI demand can get stranded, the costs pass through to utility customers, and the correction ripples outward beyond the technology sector.

Back to the beginning

Every historical infrastructure cycle has its NTT DoCoMo — the pioneer of the industry. Japan’s DoCoMo had launched the world’s first 3G service before the European auctions even began. European operators bid as if they would all benefit as much as DoCoMo. Most didn’t. While the infrastructure was being built, the returns became less attractive.

In AI, that question remains genuinely open — and the pioneer parallel is not really applicable. DoCoMo succeeded precisely because it had everything set up before European competitors even committed capital. The pioneer of the AI market seems obvious: OpenAI. However, there are many aspects to the AI sector beyond just LLMs.

Amazon is the other candidate — not as a pure AI company, but as the company with the largest data center experience, and the clearest evidence that cloud revenue can bring profits. On the other hand, AWS’s capital expenditure as a share of AWS revenue has already exceeded 75%.

Amazon is the other candidate — not as a pure AI company, but as the company with the largest data center experience, and the clearest evidence that cloud revenue can bring profits. On the other hand, AWS’s capital expenditure as a share of AWS revenue has already exceeded 75%.

The DoCoMo analogy may not name a single winner. It can only describe a feature that two or three players develop, and the rest don’t.

AI’s physical constraints add a ceiling that the 3G story never had. Data centers don’t just consume capital. They consume electricity equivalent to that of small cities and water at a comparable scale. Both put a ceiling on how fast the infrastructure can be built, regardless of how much money is invested. In mobile networks, you could put a mast almost anywhere. Data centers require power, water, land, and planning permission in places where all four are simultaneously scarce and increasingly contested.

The strategy is simple. In the summer of 2000, the executives in the auction room were betting large sums to acquire licenses. The technology worked. The timeline — the part that determined whether investors made money or lost it, whether workers kept their jobs or didn’t, whether the companies survived or were carved up and sold — was the part they got wrong.

We don’t know which part the current generation got wrong. We do know Big Tech is spending $700 billion a year to find out.

Editor’s Note: The opinions expressed here by the authors are their own, not those of impakter.com — In the Cover Photo: A close-up of a computer board. Cover Photo Credit: Andrew Dawes