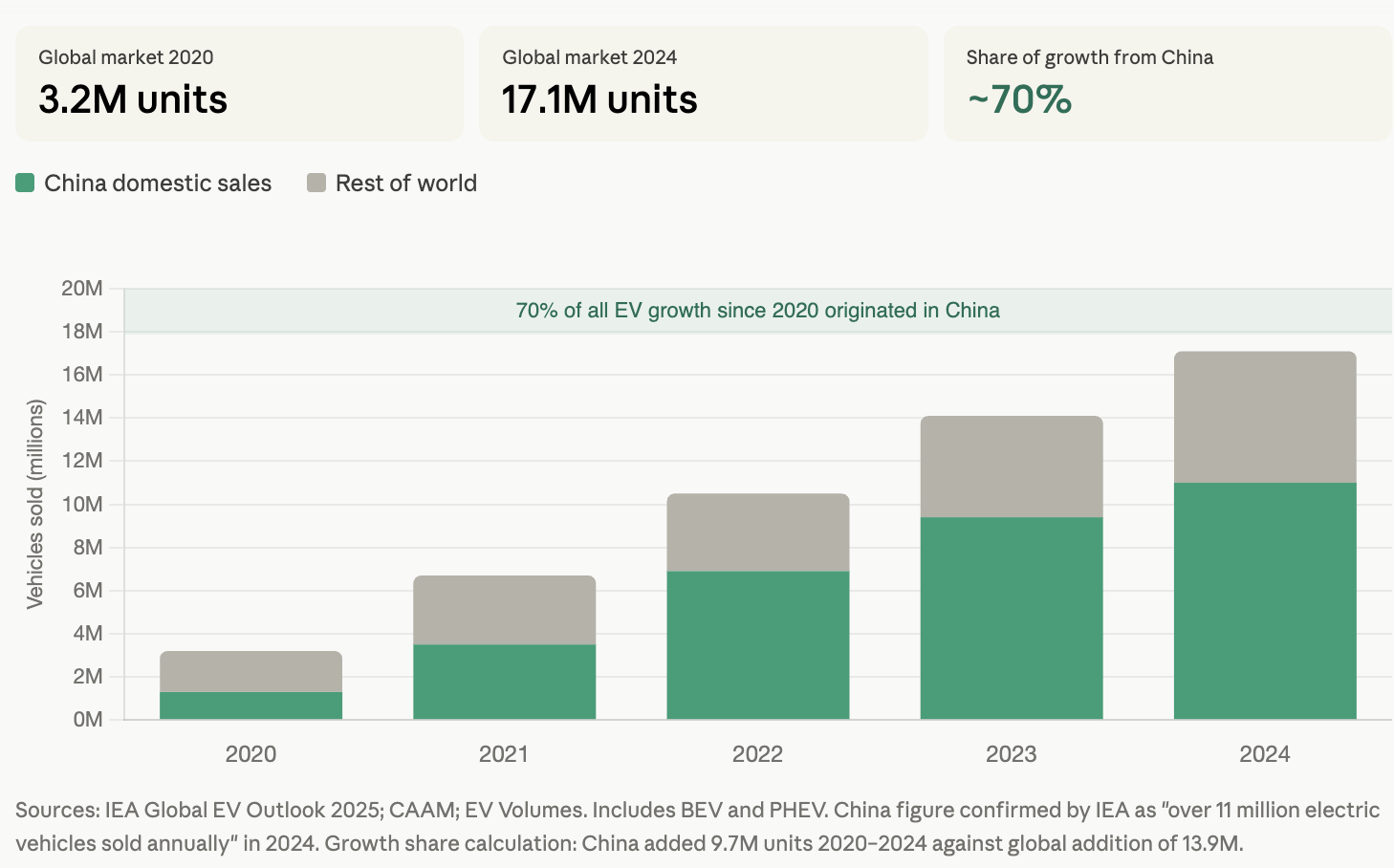

Since the start of the decade the EV market has grown close to tenfold. An amusing novelty starting to gain recognition became a worldwide craze. China has always been a key part manufacturer for electric vehicles, but now in the last decade 70% of the growth came from the Chinese market. Not parts, whole vehicles.

At the start of the decade, Chinese domestic sales accounted for about a third of total volume; now it’s closer to two-thirds. It’s the first global economy that made EVs truly affordable, debatably more affordable than traditional vehicles.

At the start of the decade, Chinese domestic sales accounted for about a third of total volume; now it’s closer to two-thirds. It’s the first global economy that made EVs truly affordable, debatably more affordable than traditional vehicles.

There are two sides to this story. One is a story about cars. The other is about industrial strategy and corporate ownership structures.

How did the EV market end up in its present form?

At the beginning of this decade, the electric vehicle market gained traction, leading to the industry’s most productive years. New companies started popping up and growing quickly around the world.

Tesla introduced the category for mass consumers, and everyone else launched new initiatives to catch up. The Chinese carmaker BYD existed, but not in Western coverage. The Volkswagen Group announced ambitious EV transitions. The Chinese domestic market was large but treated in the West as a separate contest.

That started changing between 2022 and 2023.

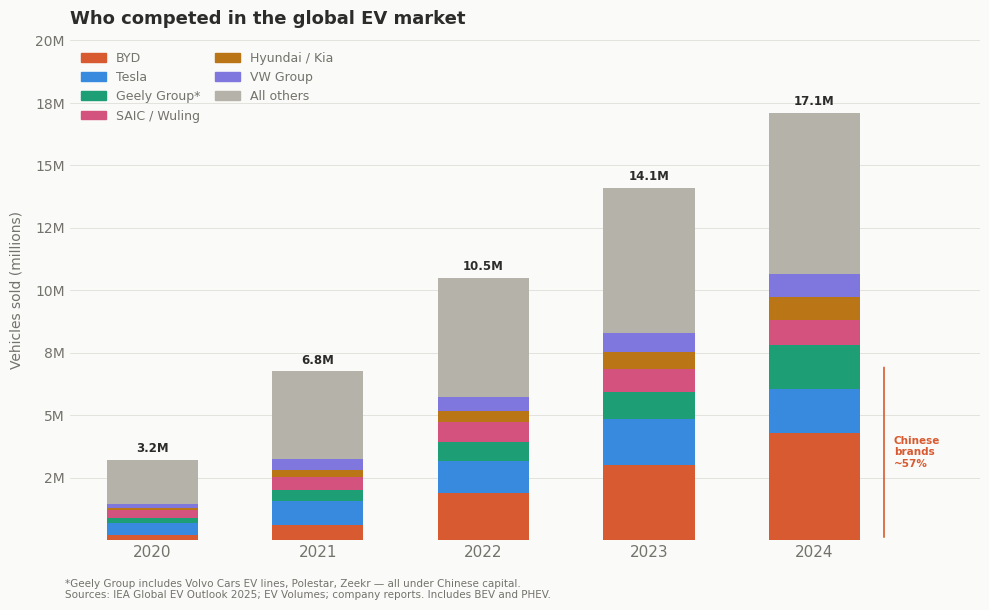

The above diagram shows how much the market has changed since the start of the decade. The detail most observers have missed is that, as the market grew, it was increasingly taken over by a smaller number of the largest manufacturers, while small brands tended to shrink or disappear.

The above diagram shows how much the market has changed since the start of the decade. The detail most observers have missed is that, as the market grew, it was increasingly taken over by a smaller number of the largest manufacturers, while small brands tended to shrink or disappear.

Chinese brands — led by BYD and others from SAIC to Geely — moved from holding roughly one-fifth of the global market in 2020 to more than half by 2024.

Meanwhile, Volkswagen Group, Hyundai, and Kia, which had bet correctly on quality-focused EVs, made genuine progress in Western markets but remained structurally dependent on US policy decisions beyond their control.

The fragmentation that characterized the 2022–2024 period was not a sign of competitive health. It was evidence of an industry in the midst of a structural shift — with most Western incumbents still figuring out which direction it was moving.

Volkswagen’s failure was viewed as a strategy problem when it was in fact a software problem. Its in-house Cariad division burned through nearly €12 billion, delayed critical Audi and Porsche models by almost two years, and released vehicles whose screens went dark while driving.

The deeper issue was efficiency, compounded by peer pressure: Chinese automakers like BYD could develop and launch new models in 18 to 24 months, whereas Volkswagen’s global development cycle typically ran between 3 and 5 years. In comparison, over the same time frame, Chinese manufacturers delivered on their promises, while Volkswagen seemed either slow or rushed.

Hyundai and Kia’s diagnosis is almost the inverse.

The products were right: the IONIQ 5 and EV6 were genuinely competitive vehicles that found real buyers in Western markets. Then came the Inflation Reduction Act, which immediately eliminated the $7,500 consumer tax credit for EVs imported from outside North America. Both manufacturers lost their pricing edge overnight.

Trump-era tariffs then added an estimated $5 billion in additional annual costs. When the federal EV tax credit expired at the end of September 2025, both brands’ EV sales dropped by more than 50% in a single month — the Kia EV6 alone fell 71% year-on-year.

Volkswagen built the wrong car. Hyundai and Kia built the right cars in the wrong supply chain.

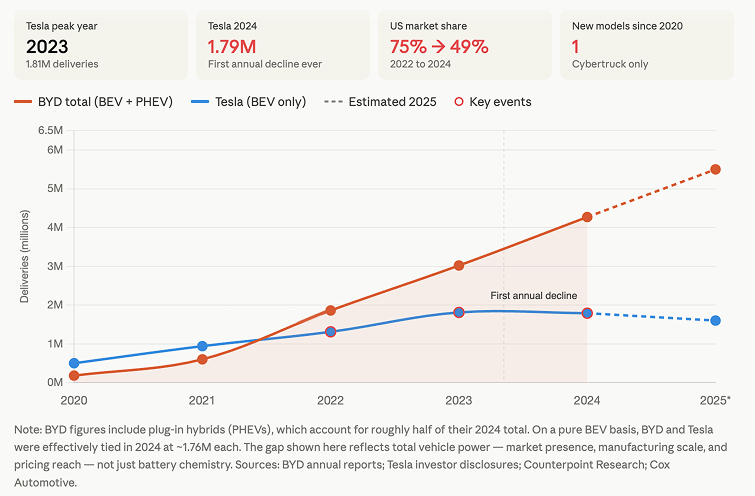

All the factors related to tariffs and regulations in the US must have benefited Tesla, its largest domestic player. For most of the 2010s, its story was one of implausible success.

Tesla, an iconic Silicon Valley startup, not only managed to build electric cars but convinced enough people to buy them at a price premium. By 2022, Tesla held roughly 75% of the US EV market. No other car company had ever achieved that kind of dominance in a major industry segment.

In 2024, that share had fallen below 50%. And 2024 was the first year in Tesla’s history in which annual deliveries declined — albeit barely, from 1.81 million to 1.79 million; but the direction itself was enough to cause worry. In the first half of 2025, the decline steepened: consecutive quarters of double-digit sales drops, including what the company acknowledged was its worst-ever quarterly result.

The first issue concerns the products. The Cybertruck is the only new model since 2020. It was not a success: an angular, polarising pickup that proved too expensive and too offbeat to reach the masses.

Meanwhile, the core lineup — Model 3, Model Y, Model S, Model X — has aged. The competitive environment around those models became much fiercer. In 2020, Model 3 buyers had few serious alternatives. By 2024, they had many.

The second problem is the company founder, Elon Musk. His increasingly controversial political visibility caused significant brand damage in European markets and, to a lesser degree, in the US. Sales figures in markets like Germany and Australia showed drops that correlated with his political activities, proving that the products were not the only issue.

The tariff regime that blocks Chinese EVs from entering the American market has been the only protector of Tesla’s US position.

BYD’s Seagull hatchback costs just $10,000 in its home market — commercially unviable in the US at a 100% tariff rate. Without this barrier for fair competition, Tesla’s US market share would look considerably worse than it does. Paradoxically, the company is a beneficiary of the protectionist policy it publicly declines to endorse, not to appear as a supporter of any political camp.

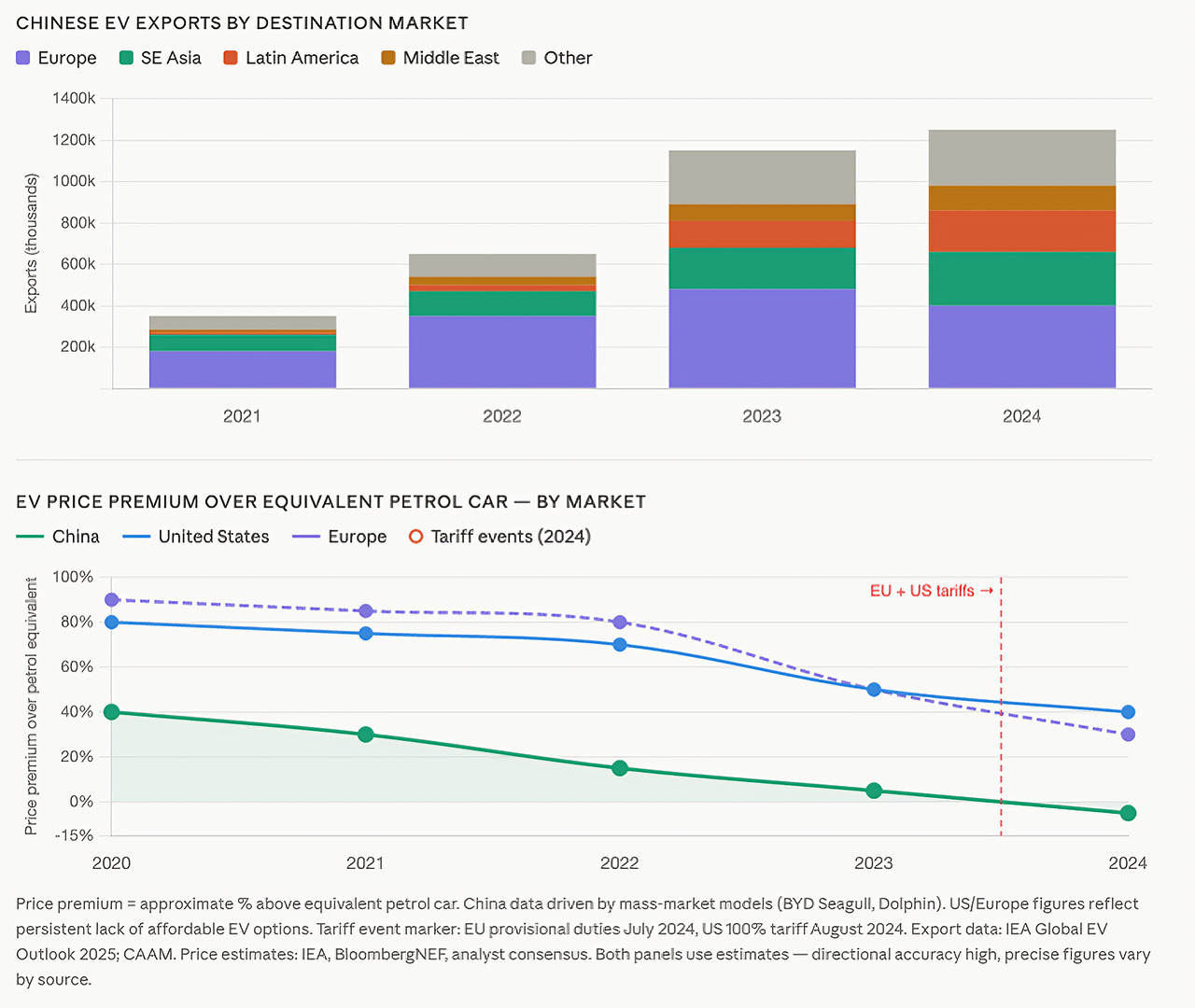

The prices of electric vehicles and how tariffs affect them

BYD can build and sell a car for less than most Western manufacturers can source their components. This fact alone justifies tariffs, but the story is more complicated, and there are caveats to how governments enforce them.

BYD started as a battery manufacturer in 1994. It began making cars in 2003, specifically to have a captive customer for its own batteries. The result is a company that controls its own battery chemistry, cell manufacturing, battery pack design, electric motors, power electronics, and vehicle assembly.

When the costs of EV components are always treated as internal transfer prices, your cost structure and margins look very different from those of a competitor who can’t produce their cars without outsourcing.

By 2024, BYD’s EVs had reached price parity — or even below — with equivalent petrol cars in the Chinese domestic market.

This was not the case in the United States, where the average EV still costs roughly 40% more than an equivalent petrol vehicle. And not the case in Europe, where the gap has narrowed from roughly 90% in 2020 to around 30% in 2024, but remains significant.

According to the latest news, BYD started focusing on exports as a result of weaker domestic demand, subsidy cuts, and fiercer competition. The company recorded the biggest quarterly drop in profits since 2020 in the first quarter of this year. It reported a 55% drop in net profit and a 55,84% rise in exports, with trial production beginning in Hungary in hopes of avoiding EU import duties, while the US market remains blocked by 100% tariffs.

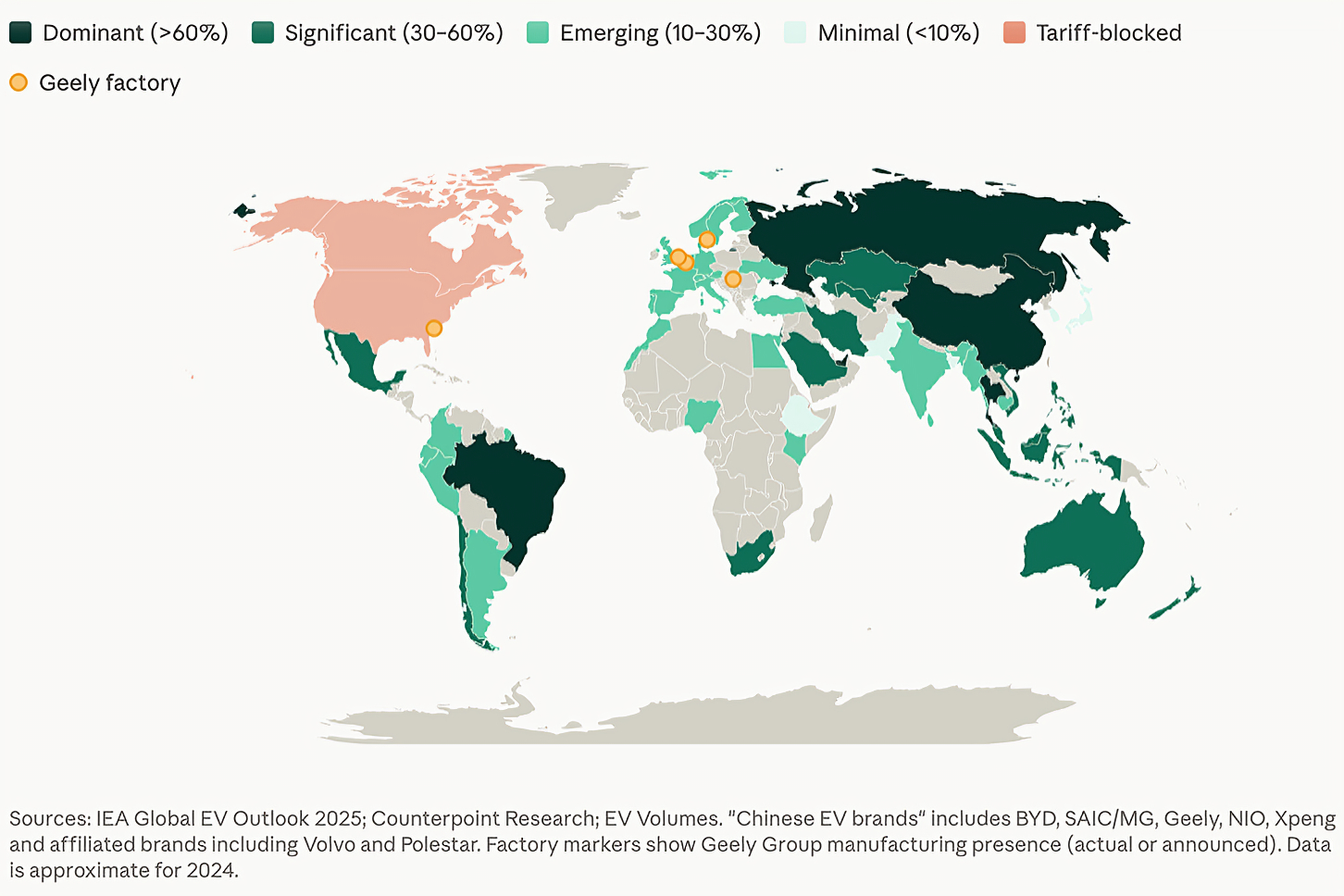

A manufacturer sitting at cost parity with petrol can enter any market, at any time, at a price that works for mass-market consumers. That flexibility explains something that is often lost in discussions of tariff policy: Chinese EV exports did not decline meaningfully when the EU and the US imposed duties in 2024. They just started rerouting because there was demand elsewhere. European volumes dropped; Latin American and Southeast Asian volumes absorbed almost the same numbers.

Brazil, where Chinese imports reached 85% of total EV sales in 2024, saw the EV price premium over petrol fall from over 100% to 25% in a single year. Thailand, Indonesia, and Mexico followed similar trajectories. The tariff created a geographic detour, not a competitive barrier.

As can be seen in the diagram above, even in the tariff-blocked US, Geely has some reach through a Volvo capacity in South Carolina. In Europe, EVs emerge despite tariffs (more on that later)

The European Union’s decision to impose duties of up to 45% on Chinese-made EVs in 2024, and the Biden administration’s move to raise US tariffs on the same vehicles from 25% to 100%, were initially aimed at addressing unfair Chinese subsidies. Chinese manufacturers receive state support that Western manufacturers do not, creating a price advantage that does not reflect genuine competitive efficiency. Tariffs were sufficient to neutralize that advantage.

The Chinese state invested more than $29 billion into EV subsidies, R&D, and tax breaks between 2009 and 2022. A manufacturer competing without equivalent state backing is at a disadvantage. However, the price advantage of Chinese EVs is only partially attributable to subsidies. The vertical integration and manufacturing efficiency described above would persist regardless of the removal of subsidies.

The tariffs protect existing manufacturers rather than incentivizing the development of competitive alternatives. Tariffs do not cause Volkswagen’s difficulties in China — they are caused by Chinese manufacturers building better, software-defined vehicles at a lower cost and faster.

The tariffs protect existing manufacturers rather than incentivizing the development of competitive alternatives. Tariffs do not cause Volkswagen’s difficulties in China — they are caused by Chinese manufacturers building better, software-defined vehicles at a lower cost and faster.

The main point is this: A tariff on Chinese imports into Europe does not help Volkswagen solve that problem.

Third — and this is the mechanism the tariff was not designed to address — the most sophisticated Chinese automotive capital does not need to export cars into Western markets at all. This is the subtle, winning strategy adopted by the Chinese and exemplified by what happened to Volvo, as explained below.

Related Articles

Here is a list of articles selected by our Editorial Board that have gained significant interest from the public:

Market control in shadows, or how Geely Holding evades tariffs?

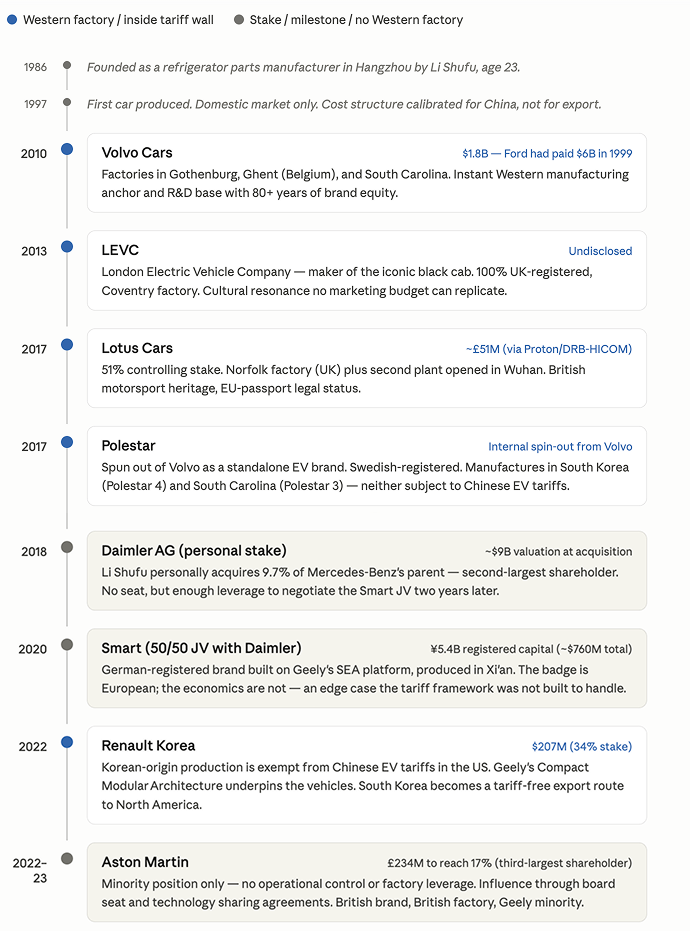

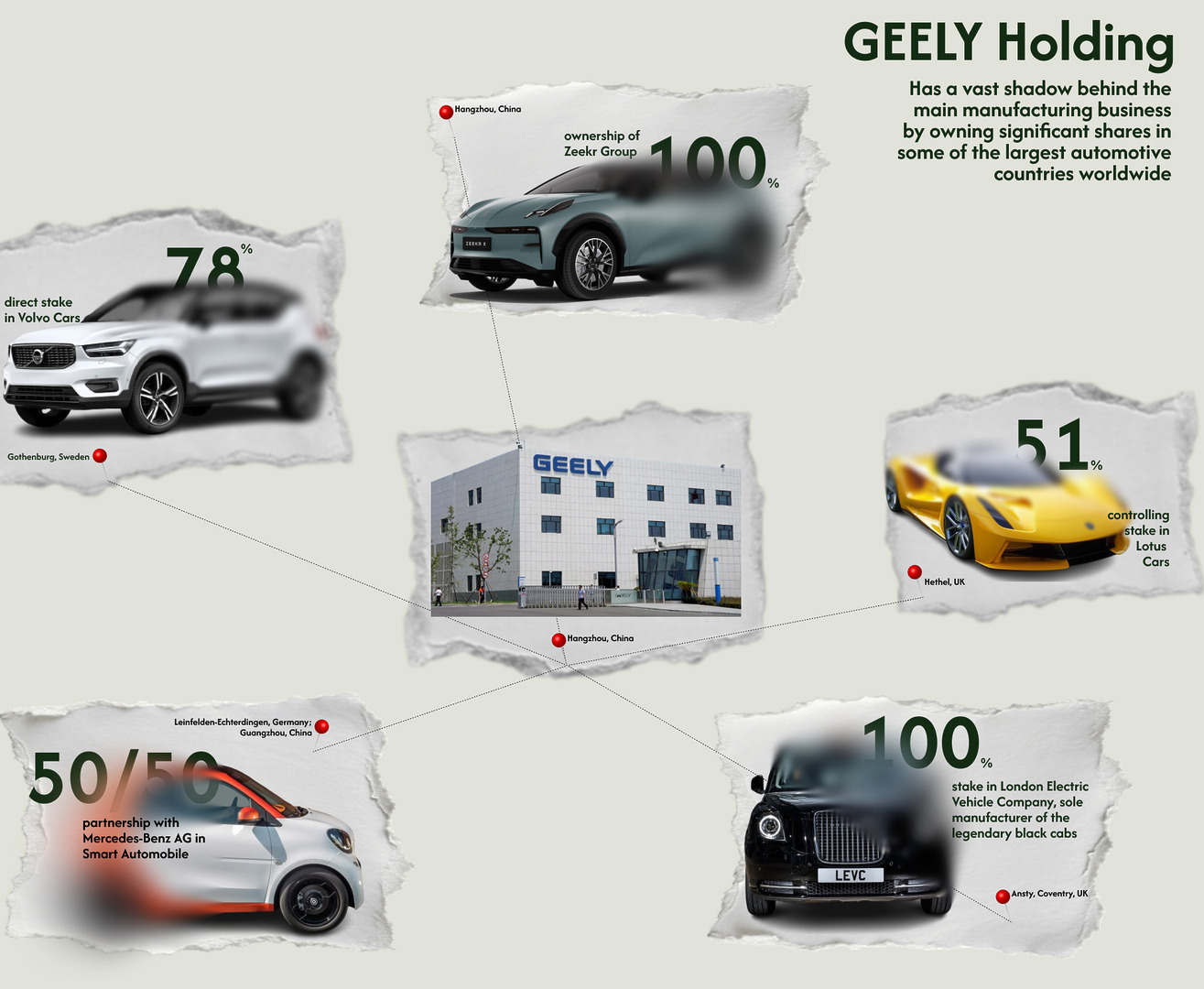

Zhejiang Geely Holding Group is headquartered in Hangzhou, China. It was founded in 1986, began making cars in 1998, and spent the first decade of this century as an unremarkable domestic manufacturer. Then, in 2010, it purchased Volvo Cars from Ford for $1.8 billion.

Geely did not buy Volvo to extract its assets or reduce it to a badge on Chinese-built hardware. It invested in Volvo’s engineering, preserved its Swedish identity and expertise, and used the relationship to build something more valuable than a brand: a European manufacturing and legal footprint.

Volvo has factories in Sweden, Belgium, and South Carolina. It has R&D operations in Gothenburg. It employs thousands of European engineers and designers.

Under Geely’s ownership, Volvo’s second-generation XC90 became genuinely competitive with German premium rivals in ways it had not been under Ford. This experience started a network of daughter companies and partial ownerships to create one of the most powerful companies in the automotive industry.

Under Geely’s ownership, Volvo’s second-generation XC90 became genuinely competitive with German premium rivals in ways it had not been under Ford. This experience started a network of daughter companies and partial ownerships to create one of the most powerful companies in the automotive industry.

Over time, Geely Holding acquired a portfolio of car manufacturers around the world that enables it to influence the whole market

Through Volvo, Geely holds a 48% stake in Polestar — a Swedish-registered EV company that, depending on the model, manufactures in China, South Carolina, or South Korea.

Geely separately acquired a 51% stake in Lotus Cars, the British sports car manufacturer, which now operates factories in Norfolk, England, and Wuhan, China. It purchased the London Electric Vehicle Company, manufacturer of the iconic London black cab, giving it 100% ownership of a UK-registered company with cultural resonance.

Through a joint venture with Mercedes-Benz, it co-owns Smart Automobile, which holds German registration despite producing vehicles in Xi’an.

Smart is an extreme case the tariff framework was not designed to handle: a German-registered brand, joint-owned with Daimler, built on Geely’s SEA platform, manufactured in Xi’an. The tariff applies to Smart, but Geely’s brand equity is not tied to it.

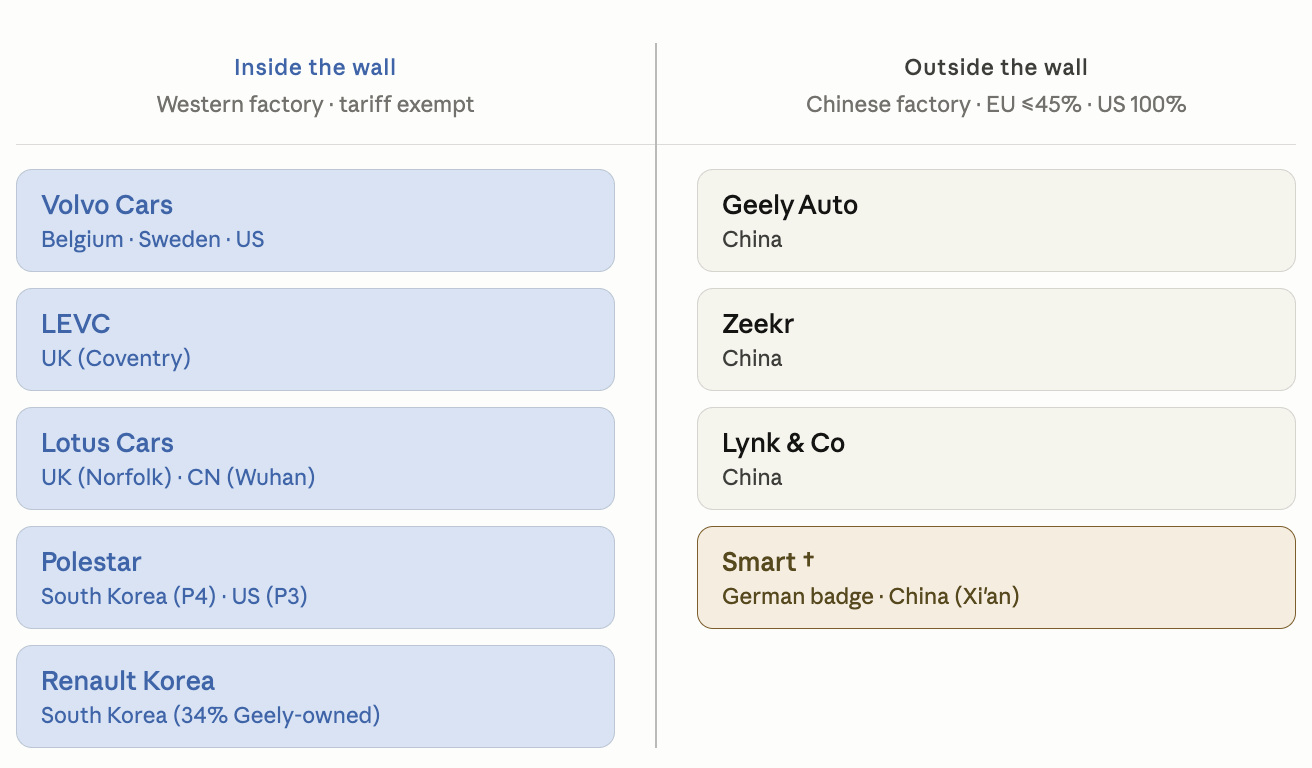

The result is a Chinese holding company that controls, through majority stakes, five automotive brands with European or British legal identities.

Consequently, it now has a manufacturing presence inside the tariff wall and consumer reputations built over decades of independent Western operations. A buyer purchasing a Volvo EX40, a Polestar 3, or a Lotus Eletre is buying a product whose profits ultimately flow to Hangzhou, whose platform engineering was directed by Geely, and whose competitive pricing reflects, at least in part, access to Chinese manufacturing economics. The tariffs’ design blocks Chinese EVs, not Chinese capital.

Geely is now moving further. The company has announced plans to manufacture Zeekr models at Volvo’s European facilities, thereby making them legally European-manufactured and exempt from import duties. It has considered using Volvo’s South Carolina plant to produce non-Volvo models for the US market. The Polestar 4, which shares most of its engineering with the Zeekr 001, is produced in South Korea precisely because Korean-origin vehicles are exempt from the Chinese EV tariff.

None of this is illegal. None of it is even particularly opaque — the ownership structures are transparent, and make headlines when deals finalize. It is simply a more sophisticated version of the same industrial strategy that built Chinese EV dominance in the first place: identify where the competitive advantage lies, structure around the constraints, and compete.

What comes next, and what we cannot predict

The EV market in 2026 looks nothing like it did in 2020. BYD is the world’s largest electric vehicle manufacturer by total volume — an underdog at the decade’s start, with presence mainly on the domestic market.

Tesla remains the dominant brand in Western premium EV segments. Still, its narrative of inevitable platform dominance has been replaced by a more ordinary story of a maturing company facing genuine competition. They now control less than half of the US market; the psychological perception of dominance is gone.

European legacy manufacturers are caught between an EV transition they cannot afford to abandon and Chinese competition they cannot yet match on cost. The tariff wall, built at considerable political effort and economic cost, has demonstrably redirected Chinese exports without reversing Chinese competitive advantage.

Whether the software ban — the US rule prohibiting Chinese-connected vehicle system components by 2027, extending to hardware by 2030 — proves more effective than the tariff is the open question. It targets the actually valuable layer: the algorithms, the over-the-air update architecture. The details that would make even Geely’s daughter companies pay.

Geely itself acknowledges that losing Chinese software would make its Western-branded vehicles meaningfully worse. That is a different kind of constraint than a price on steel and glass.

The deeper uncertainty is whether Western industrial policy can accelerate domestic EV competitiveness faster than Chinese manufacturers can restructure around the next barrier.

In recent experience, the second outcome seems more likely. The wall gets built; the door gets found. The question is whether there is a version of this contest in which the West competes on the same terms — or whether the structural advantages accumulated over a decade of Chinese industrial strategy have already determined the outcome.

That question does not yet have an answer. The cars, however, are already on the road.

Editor’s Note: The opinions expressed here by the authors are their own, not those of impakter.com — In the Cover Photo: Police Cars, operating in Shenzhen Cover Photo Credit: The Transport Enthusiast DC