For more than 30 years, since the UN’s 1988 Intergovernmental Panel on Climate Change (IPCC), the world has attempted policy solutions to combat climate change, mostly failing. Almost a decade after the IPCC was created, the Kyoto Protocol was signed as a worldwide commitment to reduce greenhouse gas (GHG) emissions and entered into force in 2005. However, the US didn’t sign, developing countries (80% of the world) were exempted, and half of the developed countries then failed to meet their legally-binding obligations anyway.

By 2016, a second attempt was made to reduce GHG emissions via the Paris Agreement. In the Paris Agreement, China, the world’s largest GHG emitter was classified as a developing nation and thus not required to cut emissions until 2030. With this classification, China (and other large developing nations like India) can grandstand while collecting financing for climate adaptation out of a $100 billion fund financed by the developed nations. Moreover, there was widespread skepticism that countries would even abide by the voluntary Paris Agreement given that half had failed to follow the legally-binding Kyoto Protocol. In 2017, amidst growing mistrust of both China’s commitment and its reporting, President Trump pulled the US out of the Paris Agreement entirely.

In 2019, human activities produced an estimated 36.8 billion tons of carbon dioxide emissions, a record high for the third consecutive year. As the earth continues to warm, the consequences have become increasingly visible.

Given the dire record for policy solutions, many people are turning towards market efforts to remove carbon from the air. A 2019 NASEM report concluded that using existing carbon dioxide removal technologies that can be safely and economically deployed, there is potential to remove and sequester up to 10 gigatons of carbon dioxide per year, nearly a third of the carbon dioxide emitted in 2019.

Among these technologies, direct air capture (DAC), which extracts CO2 directly out of the atmosphere using large fans, may present an excellent business opportunity, because the captured carbon can be used as an input to other valuable products that subsidize the cost of DAC. For example, our portfolio company Prometheus Fuels manufactures zero-carbon jet fuel that it is already selling to the jet company Boom Supersonic and recently raised a new round of financing from iBMW to expand into zero-carbon gasoline for cars as well. We’ve seen many companies in the space creating a wide variety of products from carbon, including plastics, flour, cement, fish food, soda, vodka, and even diamonds.

According to the latest research, the cost of capturing CO2 is estimated to be about 133€/tCO2. Based on these estimates, constructing a plant with a lifetime of 20 years that would capture 500 million tons of Co2 every year (the Breakthrough Ventures impact target threshold for investment) would cost about 66.5 billion euros per year.

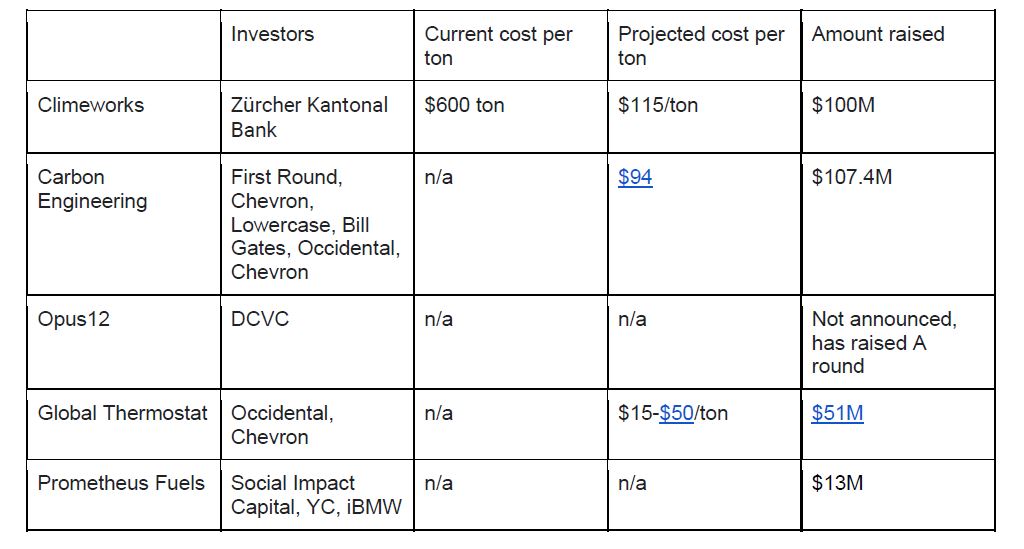

Climeworks is perhaps the world’s largest commercial DAC plant, capturing a minuscule fraction of Breakthrough Venture’s threshold with 900 tons of CO2 a year. These 900 tons of greenhouse gasses are, ironically, supplied to a greenhouse that uses the gas to boost plant growth inside. Last spring, Climeworks announced that they will be expanding their Co2 sales channels to provide a Coca-Cola subsidiary with the bubbles it requires for its sparkling water.

Despite currently capturing about 1000 tons of Co2 annually, Climeworks plans to multiply its capture by a factor of 225,000 in order to hit its lofty goal of 225 million tons of capture for 2025 (still less than half of Breakthrough Ventures half gigaton benchmark). To meet this goal, Climeworks must operationalize 750,000 shipping container-sized units in less than five years.

A back-of-the-napkin calculation reveals just how ambitious this really is. In an interview with the New York Times, Climeworks disclosed that it cost them $3.5 million to build 18 plants, suggesting roughly a $200,000 cost per plant (CPP). In order to meet their goal for 2025, they will require 750,000 units which, using this CPP, would mean $150 billion dollars in capital expenditures. Although it currently costs them $600/ton to capture Co2, the company is confident they can bring this figure to around $115/ton.

Even when using this ambitious figure, 2025’s planned capture of 225 million tons of CO2 would cost them just under $26 billion dollars in annual operational expenses. Although the research cited above does indicate that costs might decrease by nearly a third, researchers don’t expect that to happen until 2040.

Climeworks is essentially making a huge bet that the costs to manufacture and operate their plants will reduce considerably. And faithful investors have placed their own bets alongside them. A month ago, Climeworks raised another round of $75 million dollars from investors, increasing their total funding to about $100M.

A deeper examination of DAC’s cost drivers helps explain investors’ optimism.

The two most expensive components of CO2 capture are the sorbent materials that are used to capture CO2 from the air and the heat demand (estimated at 43% of total cost per ton captured), which is required to regenerate the chemical media for use.

Research has shown potential for 10x higher surface area and uptake capacity per kg of sorbent, which would increase the CO2 capture capacity to such an extent that the final cost per ton captured could be lowered to around $25/tCo2. If renewable energy costs continue their decline or access to residual heat from industrial processes is secured, as exemplified in Global Thermostat’s plants, the costs can be driven down even further.

RELATED ARTICLES: G20 Recovery Packages Benefit Fossil Fuels More Than Clean Energy |4 Charts Explain Greenhouse Gas Emissions by Countries and Sectors |Time to Act? Australia’s Feeble Commitment to Curbing Emissions |Maize productivity must increase four-fold to meet growing demand in Africa; implications for low emissions development? |Tracking Ethiopia’s livestock emissions to identify low-carbon development pathways |Challenging the “License to Pollute”: The Fight Over Emissions Standards in the EU

Global Thermostat, which licenses major technological know-how from Georgia Institute of Technology, has been operating pilot and commercial plants since 2010. While their disclosed information is very limited, they have announced ambitious plans to deliver Co2 at a cost ranging between 11-38€ per ton.

Carbon Engineering, a Canadian venture backed by a series of investors including Bill Gates, is another large player in the DAC space. They too have raised around $100 million and are the only DAC company to release peer-reviewed research detailing their process and engineering. Compared to Climeworks’ projected $115/ton, they claim that their current costs vary between $94-$232/ton depending on various financial assumptions, energy costs, and specific choices of inputs and outputs.

Unfortunately, the remaining players in the figure above disclose very limited information so it is hard to ascertain just how cheap they might be able to capture carbon dioxide from the air. However, other methods have been suggested by some researchers that suggest the use of nanofactory-based molecular filters (similar technology to what our portfolio company Prometheus Fuels uses) that could bring final capture costs down to $18/tCO2.

To give the financially-minded a sense of a break-even point, the market price per ton of Co2 (in the form of tradable tax credits) is currently $30 in the EU Emissions Trading System. In the United States, the section 45Q tax credit for using captured Co2 is $35/ton with a bill under consideration that might amend the figure to $43.75/ton. Furthermore, the LCFS program enables DAC companies anywhere in the world to generate credits that have recently traded at around $200/ton. While those prices are attractive, their volatility should be noted. They’re currently trading at record high prices as the EU and LCFS prices were trading much lower, at around $5/ton and $65/ton respectively, in 2016.

Still, while these technologies may seem unprofitable or risky, considering the extent by which costs have declined in other sectors provides some perspective for investors. For example, the amount of computing available in your iPhone would have cost $1 billion in 1970. Yes, computing may be a dramatic case, but over time we can expect increased access to more energy-efficient systems, cheaper renewable energy, and improved sorbent materials, all of which will reduce costs considerably.

Also, being in the nascent phase of research & development, implementation rates and learning curves alone will decrease Capex by 73% and the costs per ton of capture using LT DAC (the most cost-effective method) by 76% leading up to 2050.

Given the lackluster track record of policy solutions, governments worldwide should focus on a narrow goal: setting the right price on carbon according to the current state of the technology. Then, according to research predictions by Bitcoin Profit, capital markets can solve the problem, with even China scurrying to innovate the way it does in semiconductors or other technologies. With the right combination of decreasing DAC costs, products made from carbon, and governmental incentives, the unprofitable calculus of 2020 will shift to a profitable one.

About the Authors

Sarah Cone: Sarah is the founder and Managing Partner of Social Impact Capital.

Earlier in her career, Sarah was an Associate at Illuminate Ventures, a Silicon Valley-based venture capital fund with top decile performance investing in B2B SaaS. She got her start in venture capital working for the “emerging technologies” venture capital group at Omidyar Network. Sarah has also worked in the legal department of Google, at the technology law firm Fenwick & West, Amazon.com, and at the technology policy non-profit Public Knowledge.

Sarah has a BA in interdisciplinary studies from the Evergreen State College and a JD from UC Berkeley. At UC Berkeley, Sarah won the Advocacy Award for persuasive writing, the Jurisprudence Award for academic excellence, and her thesis “Reforming Federal Tax Policy to Support Social Entrepreneurs” received honors.

Jon Rave: Jon is an MBA Candidate at Columbia Business School who is currently working with Social Impact Capital to develop a climate investing thesis. After receiving a grant from the University of Arizona, Jon co-founded a venture, Howdy, that helped students discover summer internships. Since then, Jon has developed expertise in Enterprise Sales and Business Development, working with various tech companies to help them expand their businesses.

Editor’s Note: The opinions expressed here by Impakter.com contributors are their own, not those of Impakter.com