Agricultural production is fundamental to improving nutrition and is the main source of income for many. Increases in crop production are key to ending hunger and to economic and social development, yet the current tensions around the Strait of Hormuz are sparking fears of skyrocketing food prices, as nearly 1 million metric tonnes of urea and fertilisers pile up in Gulf ports and energy-driven costs surge across the food chain.

For reference, the Strait of Hormuz is only 29 nautical miles wide (54 km) at its narrowest point, and it consists of 2-mile-wide navigable channels (3.7 km) for inbound and outbound shipping as well as a 2-mile-wide buffer zone. Despite the narrowness, the strait handles 20 million bpd (barrels of oil per day), 25% of global seaborne oil trade, with about 80% of those flows destined for Asia; 19% of global LNG, including about 93% and 96% of Qatar’s and the UAE’s LNG exports respectively; and 44% of total global sulphur exports.

With the strait being blocked, urea prices have risen by over 30%; Brent crude prices rose to over 100$/bbl (per barrel), and the Japan/Korea Marker LNG prices (Asian LNG price benchmark) rose to over 20$/MMBtu, amplifying energy costs for fertiliser production reliant on oil and natural gas, which already accounts for 70-90% of ammonia synthesis expenses. Furthermore, phosphate rock shipments from Morocco and Jordan are rerouted around Africa, resulting in delays of up to 20 days and further straining supplies, increasing costs for corn and wheat crops.

Without swift intervention and amid combined inflationary pressures in a world still recovering from prior shocks such as the 2022 war in Ukraine, the shock may hit consumers more directly this time. To understand how this plays out in practice, it helps to take a closer look at how synthetic fertilisers are made, how critical they are to the modern agriculture system, and why they depend so heavily on oil and gas.

Why synthetic fertilizers are critical to modern agriculture

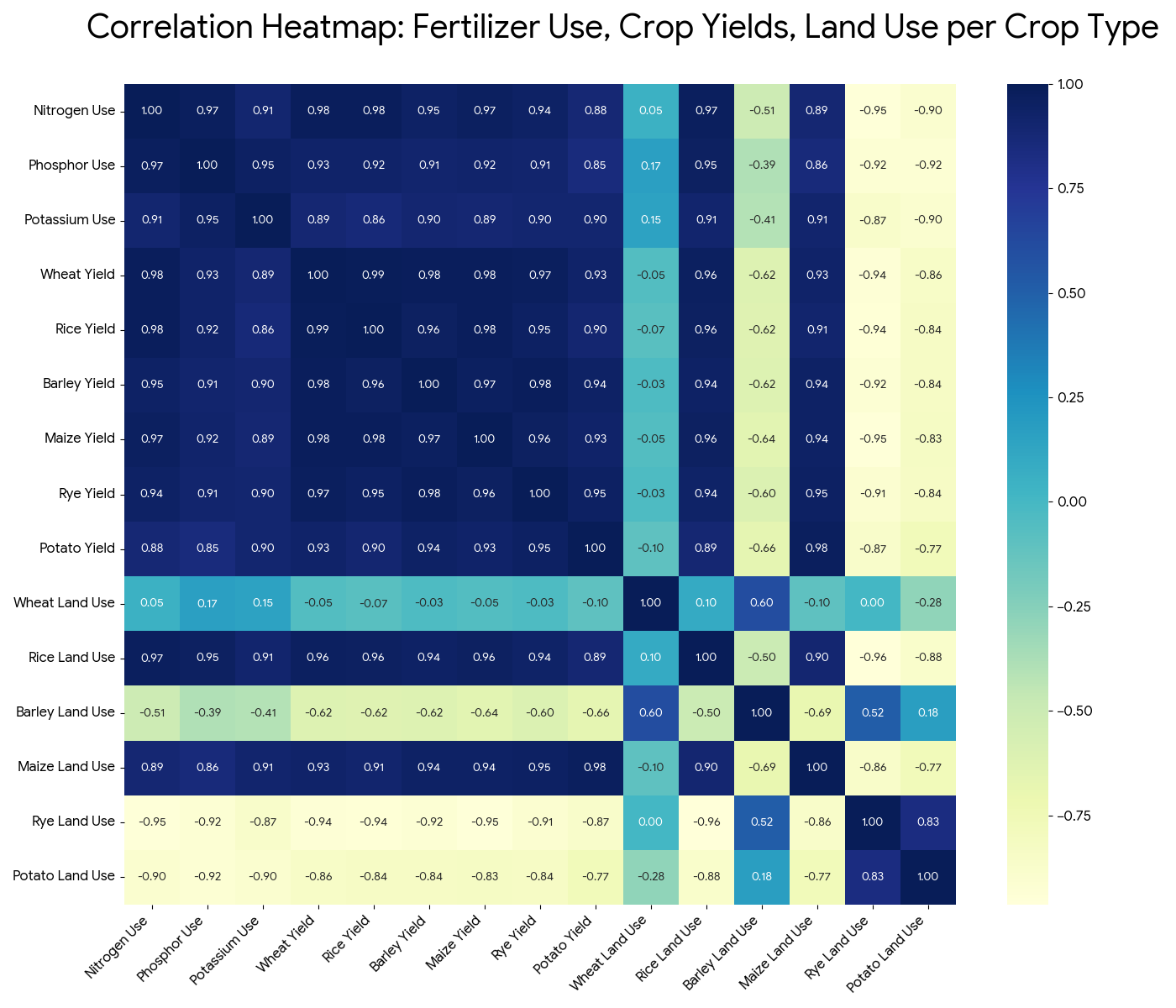

Synthetic Nitrogen, Phosphorus, and Potassium (NPK) fertilisers are industrial chemicals that revolutionised farming, delivering 30-50% yield boosts in staple crops like cereals, wheat, and maize, which feeds ~48% of humanity; hence, if the Hormuz blockade continues, we can expect the problem to worsen by hitting staple crops in India, Brazil, and the US. To show how deep this dependence runs, I draw FAO data from 1961 to 2023 to conduct a simple correlation test between fertiliser usage and crop yields, with land use as a bonus. My aim here is not to drown readers in statistics but to show how increased synthetic fertiliser use affects staple crop yields.

My analysis reveals a profound and nearly linear relationship between fertiliser use and crop yields. At the core of this relationship is the role of NPK fertilisers as the fundamental catalyst for modern agricultural output. Nitrogen-based fertiliser use shows a strong link to increases in wheat and rice production, suggesting that the massive leap in global caloric production observed over the last several decades is less a result of land-use expansion and more a direct consequence of the systematic intensification of synthetic inputs. Phosphorus- and potassium-based fertilisers follow a similar trajectory, showing consistently strong links across all crop varieties. The correlation test shows a systemic reality in which the modern agricultural engine is essentially a machine that converts chemical inputs into edible energy with remarkable consistency.

While the link between fertiliser and yield is the primary driver of the system, the resulting productivity gains have a secondary effect on global land management. This “bonus” insight into land-use patterns shows that not all crops respond to higher yields in the same way. For high-demand “expansionist” crops like rice and maize, the increase in yield is strongly linked to total land used, suggesting that higher efficiency has simply fuelled greater global investment and land conversion for these specific commodities.

Conversely, “legacy” crops such as rye and potatoes exhibit a strong negative correlation with land use. In these cases, the massive yield gains achieved through fertiliser intensification have enabled an efficiency-led contraction: as each hectare becomes more productive, the total amount of land required to meet demand has actually decreased. Ultimately, this means that the global surge in fertiliser demand is being funnelled into a narrower selection of high-expansion crops, while the land footprint for traditional staples shrinks even as their individual productivity reaches historic highs.

The energy-food nexus: why oil and gas prices dictate food bills

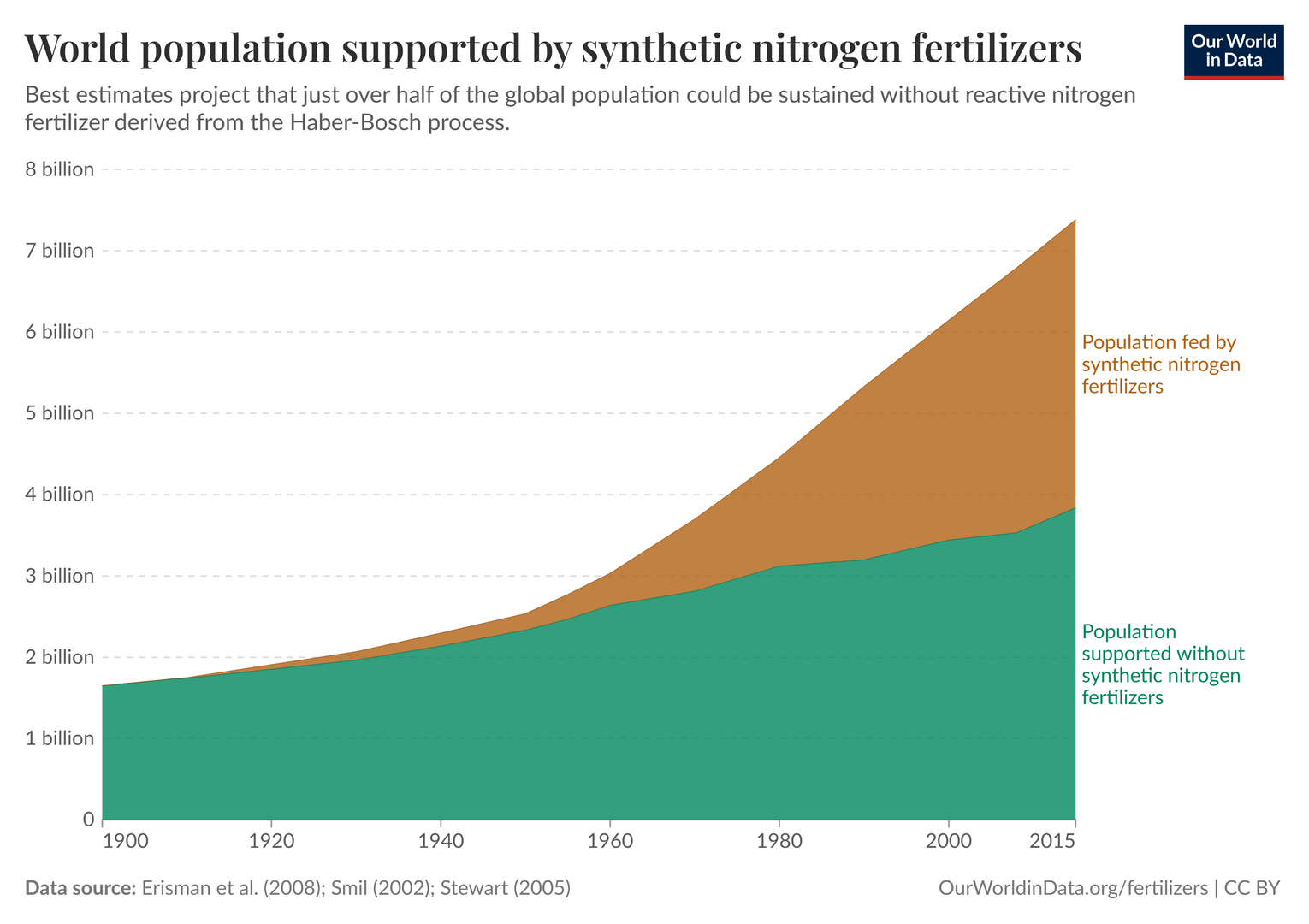

The production of these fertilisers involves complex processes like the Haber-Bosch method, which revolutionised the synthesis of ammonia from nitrogen and hydrogen, primarily derived from natural gas; the mining and processing of phosphate rock for phosphate-based fertilisers; and the extraction and refinement of kalium for potassium-based fertilisers. The demand for synthetic fertilisers comes when more natural alternatives like manure and legumes are insufficient at scale, with output limited to pre-industrial levels that can support about four billion people, slightly less than half of today’s world population.

Energy prices feed into fertiliser costs in two main ways. When gas and electricity prices spike, running gas‑based ammonia plants and other fertiliser facilities becomes more expensive, pushing up the global price of nitrogen‑based fertilisers; higher oil and diesel prices then raise the cost of transporting raw materials and finished fertilisers to farms, and the fuel needed for tractors and irrigation further tightens the energy‑fertiliser link.

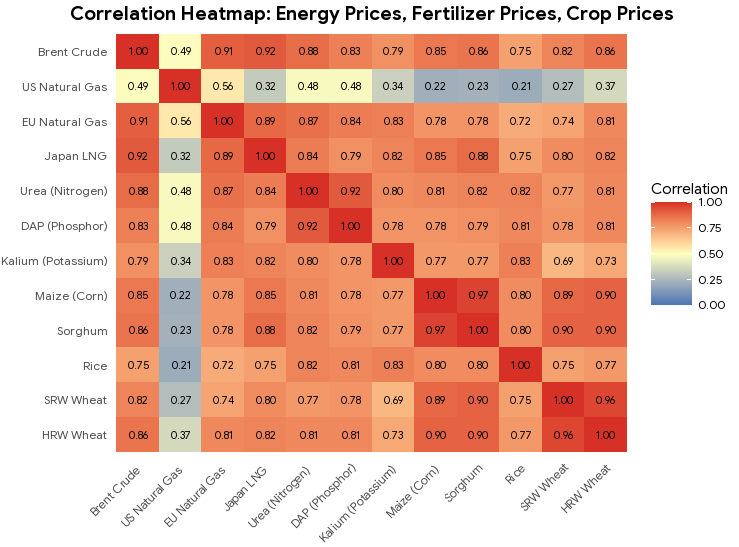

In a Hormuz‑blockade scenario, a jump in shipping and regional fuel costs would feed into farm input expenses, producer prices, and ultimately consumer food prices. Any later easing in energy markets might not fully unwind those higher food prices. To put some structure around this, I draw on data from the World Bank’s “Pink Sheet” to conduct a simple correlation test between energy, fertiliser, and food prices. I then compare the potential impact of a Hormuz blockade with previous shocks, notably the 2008 financial crisis and the 2022 Russia–Ukraine war. My aim here is not to drown readers in statistics but to show how energy shocks travel through fertilisers into food.

The commodity correlation matrix reveals a deeply integrated global ecosystem in which energy, agricultural inputs, and food prices are closely linked. Data from the World Bank “Pink Sheet” confirm that energy prices are a primary driver of fertiliser costs, as fertiliser production is highly energy‑intensive.

Brent crude and European Union (EU) natural gas stand out as the main anchors: Brent moves closely with urea and phosphorus prices, and EU gas prices show a similarly tight link to urea prices, suggesting that when global oil and gas prices rise, fertiliser costs tend to follow. Likewise, potassium prices track global oil and LNG (Liquefied Natural Gas) benchmarks, while US natural gas behaves more like a regional side story, with a much looser connection to fertiliser markets, reflecting the relative independence of the US gas market.

In the next step of the chain, fertiliser and grain prices are strongly aligned: most major cereals, from maize and sorghum to soft and hard wheat, sit in the high‑0.7s to low‑0.8s against urea and phosphorus, and rice shows an especially tight link to potassium‑based fertilisers, underlining how different nutrients underpin different staples.

The loop closes with food-to-energy links: Brent crude prices again act as a key reference point for global grain prices, and this is mirrored in the price of Japanese LNG; when oil and LNG benchmarks surge, the wider agricultural complex tends to rise as well. US natural gas again appears as the outlier, with only a faint echo in global grain prices, reinforcing the idea that it is the world‑facing energy benchmarks, rather than local US gas swings, that set the tone for international food markets.

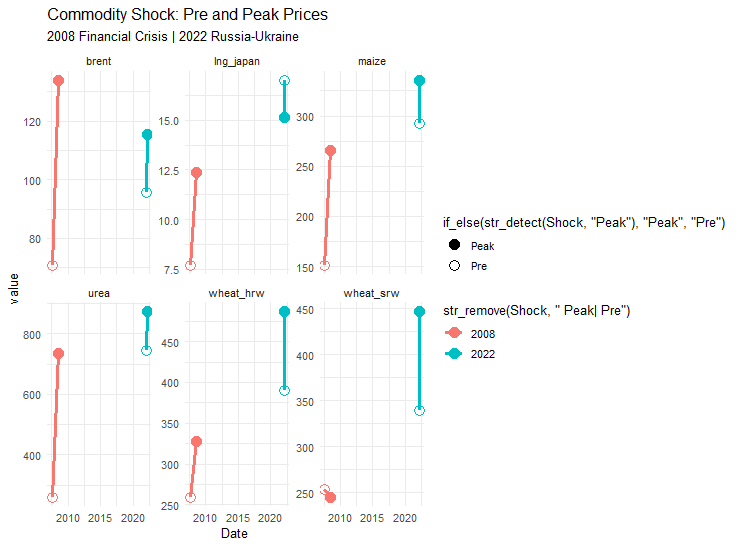

Historical shocks that turn energy spikes into food crises

Previous crises, such as the 2008 Financial Crisis (red) and the 2022 Russia-Ukraine war (blue), illustrate what happens when energy prices (specifically Brent crude) rise. With the exception of the 2022 Ukraine war’s impact on Japan’s LNG and SRW wheat prices during the 2008 financial crisis, when a shock hits, prices all go up, starting with Brent crude. For example, during the 2022 war in Ukraine, Brent crude prices rose by 20.71%, leading to higher prices for urea fertiliser, maize (corn), and wheat.

Hence, given the strong correlations among energy, fertiliser, and food, if oil and fertiliser prices remain where they are due to the blockage, prices of grains like maize and wheat are likely to rise soon.

To summarise, the current blockade is both a regional flare-up and a signal: true food security demands energy independence alongside a strong agricultural system. Until we loosen oil and gas’s hidden grip on staples, every meal carries the Strait’s risk, or any geopolitical risk for that matter.

Editor’s Note: The opinions expressed here by the authors are their own, not those of impakter.com — In the Cover Photo: The Strait of Hormuz. Cover Photo Credit: Wikimedia Commons