Once again, Facebook is shaking the world. After multiple privacy violations, with a potential $5bn fine from the US Federal Trade Commission (FTC) which opened an investigation in response to the Cambridge Analytica revelations, now Facebook has come up with Libra, a brave new cryptocurrency project.

Touted as better than any cryptocurrency to date, stable, secure, fast and protected, the Libra is Facebook’s wager that it can shake up the financial world and make it better. Make it work for the 1.7 billion unbanked people in the world. Financial regulators around the world are dubious and one thing is certain: Facebook will need to engage in battle to get its project approved.

The idea behind Libra and its digital wallet Calibra is simple enough. Sending money to a friend or paying for something will be as easy as sending a Facebook Message:

To do this, you will have to wait for the official launch next year but you can sign up for early access when it’s ready here.

In technical terms, it is far more complicated.

Many questions were answered in the 100-page white paper released by Facebook and available on its Libra organization website (not to be confused with the Libra Foundation or the Libra Group), in the Q&A session the press had with Facebook managers in San Francisco’s Mint building and in a Mark Zuckerberg post on Facebook.

While not all answers were satisfactory, a general picture emerges:

In short, the Libra is a new price-stable cryptocurrency. The Facebook whitepaper describes the project as “a decentralized, programmable database designed to support a low-volatility cryptocurrency” that will act as an “efficient medium of exchange for billions of people around the world.”

The Libra will be managed by 100 companies, the founding members, garnered by Facebook in a Libra Association based in Geneva as a not-for-profit organization, each with one vote (or 1 percent). Facebook will also have just one vote – which means it can’t control it.

An investment of at least $10 million is expected of each member, to be paid into a Libra Reserve. That money will purchase a basket of the world’s most used fiat currencies (the dollar, Euro, yen, Swiss franc…) and government short term bonds. The Reserve is expected to ensure the Libra will not be volatile like Bitcoin and other cryptocurrencies that are not backed by any reserve.

For now, there are 28 founding members. New members need to meet stringent requirements, like having a sizeable market or turnover. Let us note in passing that no bank (so far) is participating – presumably banks are leery of battling regulatory authorities.

Customers will use a digital wallet called Calibra, that will launch alongside the Libra currency on iOS and Android within Facebook Messenger, WhatsApp and as a standalone app. To get a Calibra wallet, users will have to provide a government-issued photo ID and other verification information. The ultimate objective it to offer in-store payments and integrations with point-of-sale systems like Square.

Libra, at first, will be launched using a “public-permissioned” blockchain which means that the 100 companies on the board of the Libra Association will be each assigned a “node” (servers) to validate operations on the blockchain. It uses a Byzantine Fault Tolerant consensus protocol, which makes it, in the words of its whitepaper, “extraordinarily difficult for an attacker to compromise 33 separately run nodes that would be required to launch an attack against the system.”

For techies, Libra, as of now, is in beta mode:The blockchain’s prototype launched its testnet 18 June, ahead of the official launch sometime in the first half of 2020. A bug bounty system will be developed later this year by the Libra Association in collaboration with HackerOne. The idea is to pay security researchers for identifying safety flaws and glitches. The system will eventually use the Move language, but since it isn’t fully ready yet, the Libra Association is implementing the Libra Core using the Rust programming language as it is designed to prevent security vulnerabilities.

The Libra system will transition to a public-permissionless blockchain within five years once the technical difficulties are ironed out.

I find surprising that the Move language Libra is set to use is still not ready and that it is operating in open source mode, calling in developers to help. A risky move. It is obvious that clever hackers could be tempted. In fact, the technical hurdles are still many and Tech Crunch’s Josh Constine fears that Facebook, after causing data theft, will run into a financial Cambridge Analytica scandal: “They’ll steal your money, not just your data”, he writes.

Why is Facebook Launching the Libra Now?

It may look strange that Facebook is announcing a new cryptocurrency now when it still hasn’t solved all the technical problems. And when it still has to put its privacy issues behind. Another case of “moving fast and breaking things”?

But there could be a very good commercial reason.

Facing saturated markets in the developed world, Facebook is looking to expand in the developing world where it could follow the Chinese Tencent’s WeChat model that has a highly profitable payments system built into its platform. A variation on WeChat is very much what Libra looks like. And the developing world, but especially fast-growing India, looks like the next big battleground.

Alphabet’s Google and Amazon have already set up shop in India and Facebook clearly does not want to lose the opportunity with India experiencing an explosive growth in the value of transactions. They have already jumped more than 50-fold in the past two years to 143 trillion rupees ($2.05 trillion).

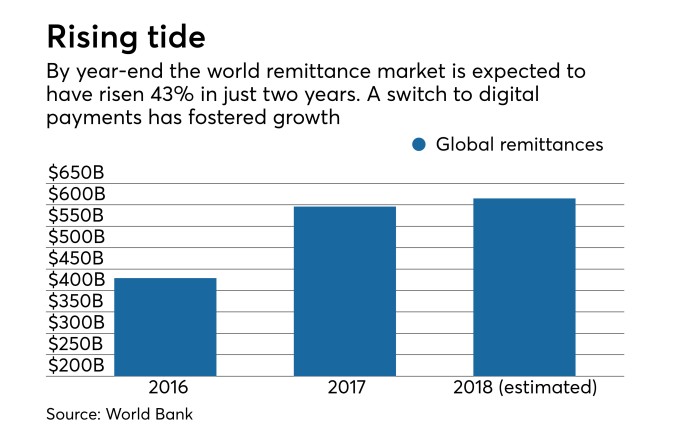

Another juicy area is global remittances. The number of people working in another country is huge and most of them send part of their salary home to family that has stayed behind.

According to World Bank data, officially-recorded remittances to developing countries reached USD 528 billion in 2018, marking an increase of over ten percent, and India is the top receiver. Remittances sent digitally, using a computer, smartphone or tablet is the fastest growing part of that market: according to a recent study (April 2019) the global market size will reach US$ 5890 million by 2024, from US$ 1540 million in 2019.

How Likely is Libra to Succeed?

Setting aside for a moment the technical difficulties Libra is facing, there are other obstacles likely to slow it down or even derail it altogether.

Following Facebook’s announcement on June 18, there were two opposite reactions. On the crypto fan side, cryptocurrency markets went up, presumably bolstered by the prospect of “the more, the merrier”. And that is fine as far as it goes.

More importantly, on the financial regulators side, a storm of doubts and criticisms arose. In Europe, regulators fear the Libra system will turn in a shadow bank, escaping all control. A sort of global tax haven, a refuge for the mafia, a colossal Cayman Islands. In the US, Representative Maxine Waters, a Democrat of California and the chairwoman of the House Financial Services Committee, reacted immediately, calling on FB to stop the development of the Libra until regulators could closely examine the potential risks.

So exactly what is it about Libra that has everyone so worried? After all, this is not the first time that a tech company nurtures a cryptocurrency project: The messaging giant Telegram raised nearly $2 billion last year to create its own cryptocurrency, which is expected in the coming months.

But Facebook is in another class than Telegram, a giant all by itself. It’s the very scale that is scary. Predictably, Facebook is sanguine about Libra. It has high hopes for it: “It feels like it is time for a better system,” David Marcus, head of Facebook’s blockchain technology research, told the New York Times. “This is something that could be a profound change for the entire world.” If Telegram were to say this, nobody would notice. But it’s Facebook saying it.

How profound could that change be?

If it worked, Libra could really change the world’s financial system. OK, that’s a big “if”, but consider what could happen, the pluses and minuses

Libra pluses compared to other cryptocurrencies:

There are seven benefits:

-

- Stability: The Libra’s value is tied to a basket of bank deposits and short-term government securities in historically stable international currencies; that is totally different from other cryptocurrencies;

-

- Ease of access: Calibra will be found everywhere on Facebook as well as through other third-party wallet apps and local resellers like convenience or grocery stores that you might already use to top-up your mobile data plan;

-

- Faster than Bitcoin or Ethereum: It is designed to handle 1,000 transactions per second, much faster than Bitcoin’s 7 transactions per second or Ethereum’s 15;

-

- Secure, scalable, fair and protected: Facebook CEO Mark Zuckerberg in his post on 18 June made it clear: “It’s decentralized — meaning it’s run by many different organizations instead of just one, making the system fairer overall. It’s available to anyone with an internet connection and has low fees and costs. And it’s secured by cryptography which helps keep your money safe”; in addition to blockchain technology, a small fee, a few cents not noticeable to users but paying the cost of running the system, will have its use to protect it from hackers; such fees, though small, make it unattractive to create the millions of transactions needed for power spam and denial-of-service attacks;

-

- Separate from FB social network to ensure privacy protection: “We realize people don’t want their social data and financial data commingled,” says Marcus, who’s now head of Calibra, “the reality is we’ll have plenty of wallets that will compete with us and many of them will not be in social, and if we want to successfully win people’s trust, we have to make sure the data will be separated”;

-

- A boost to business: The Libra Association has clearly said it wants to encourage more developers and merchants to work with its cryptocurrency “incentives”, perhaps in the form of Libra coins, to be given to validator node operators who can get people signed up for and using Libra; Libra coins could be used for business promotions; as Facebook is ubiquitous, including in markets underserved by banks, companies like Spotify clearly hope to gain from it, as Spotify’s Chief Premium Business Officer Alex Norström said, Libra coins will enable it “to better reach Spotify’s total addressable market, eliminate friction and enable payments in mass scale”; there’s a lot in it for Facebook too: (1) It hopes to grow its developer ecosystem with Libra Association founding members like Andreessen Horowitz and Union Square Ventures motivating them to fund startups to build up Libra infrastructure; (2) With a rising number of happy merchants, Facebook can expect a future boost to its ad business;

-

- Strong relationship to fiat currencies: The Libra Reserve is built one to one: as Tech Crunch explains: “Each time someone cashes in a dollar or their respective local currency, that money goes into the Libra Reserve and an equivalent value of Libra is minted and doled out to that person. If someone cashes out from the Libra Association, the Libra they give back are destroyed/burned and they receive the equivalent value in their local currency back. That means there’s always 100% of the value of the Libra in circulation, collateralized with real-world assets in the Libra Reserve.”

The last two pluses are the most problematic, something the minuses reveal.

Libra minuses

They are fewer but deeply worrying:

-

- Technical: Open source means open to shady developers: Calibra’s head of product Kevin Weil told Tech Crunch there were no plans for the Libra Association to take a role in actively vetting developers;

-

- Economic: Syphoning off fiat currencies, Libra creates a parallel economy, where blockchain provides anonymity – meaning it becomes easier to launder money or evade taxes; it also takes business away from the banking industry (unless banks decide to join in); if the use of incentives with Lira coins becomes widespread, some businesses may benefit at the expense of their rivals, for example, Uber and Lyft (both founding members) may get an additional boost further damaging competition in the taxi industry;

-

- Monetary policy: FB claims Libra Association will not engage in monetary policy – merely passively reflecting the policies of central banks in its Libra Reserve basket of currencies and short term deposits; that is disingenuous: deciding on taking in more of one currency means opening the Libra to the policies sustaining the said currency; the Libra Association, in choosing a given mix of currencies, will necessarily endorse one set of policies over another; it is far from certain the the Libra Reserve is protected from a panic or could save itself from a “bank run”;

-

- Institutional: Central banks will be faced with a new global coin (in addition to gold); governments will be faced with the world’s largest tax haven.

In the US, the news just came out that Facebook will face scrutiny over its project by the Senate’s Banking Committee on July 16. Meanwhile financial regulators in Europe, as reported today by the Financial Times, are ready with four questions:

(1) What is the Libra? If it performs banking services then it should be regulated;

(2) Are existing rules applicable or will new ones be needed? The very size of FB and potentially unprecedented concentration of financial and personal data may call for new regulations;

(3) What is the real benefit of Libra in regard to potential risks?;

(4) How likely are financial crimes, from money laundering, the top concern, to hacking and tax evasion?

The plus and minuses assumes it succeeds. For now, this is not certain, it’s still early days. Many technical and regulatory hurdles are in the way. It’s a long term project. By its own admission, it will take five years. Five years in which the regulatory system for cryptocurrencies will need to be sorted out.

Libra may just be the challenge to force G7 finance ministers and central bankers to at last take the problem of cryptocurrencies seriously and come to terms with it.