Green finance, the primary way for the financial industry to promote environmental protection and sustainable economic and social development, faces greenwashing. This means that low-cost funds from green financing are used for non-green projects.

This article starts with the explanation of the greenwashing phenomenon and its harm to the green financial market. Then, it explains the present situation of green investments and highlights the three aspects that the green market needs to work on: precise definitions, better third-party verification, and higher-quality information disclosure. Finally, I will share my opinion on distinguishing green projects in the capital market.

Related topics: Financing the Sustainable Development Goals – Ethical and Financial Investing– Impact Investing Combating Climate Change – Business Sustainability

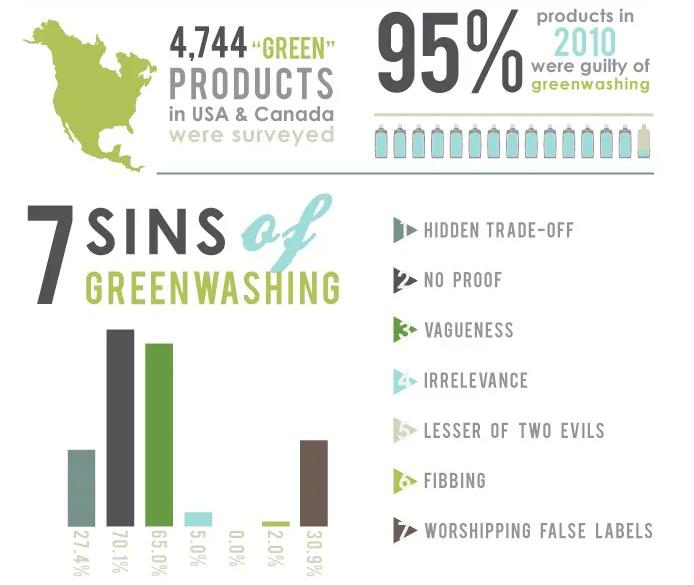

A Review of Greenwashing at the Business Level

In 1986, Jay Westerveld, an American environmentalist, pointed out greenwashing from his travel experience in Fiji. The local hotel advised customers to protect the local sea areas and coral reefs by repeat using towels. However, the hotel’s actual goal was to cut costs. The hotel’s extensive expansion near sea areas and coral reefs also reflect its pursuit of economic benefits, rather than environmental benefits. Jay calls greenwashing the act of presenting protecting the environment with the main purpose of increasing profits. In 2010, greenwashing was officially included in the Oxford English Dictionary.

Companies greenwash to make profits by catering to the orientation of public value, spreading misleading propaganda, and then misleading the masses.

Greenwashing in Finance: Using Low-Cost Green Funds for Projects with Little to no Green Benefits at All.

Green finance, as a primary way for the financial industry to help with the sustainable economic and social development, has developed rapidly in recent years, and it has great prospects.

Environmental risks change frequently in the process of climate-changing, creating a higher demand for investments in solutions. Socially Responsible Investments (SRI), which incorporates social and ecological factors into evaluation indicators, has become a preferred investment field. Socially responsible investors believe that such investments can prevent financial risks that are arising from underlying environmental and social problems.

With this new “trend” in the capital market, problems would inevitably arise. Greenwashing is one of them.

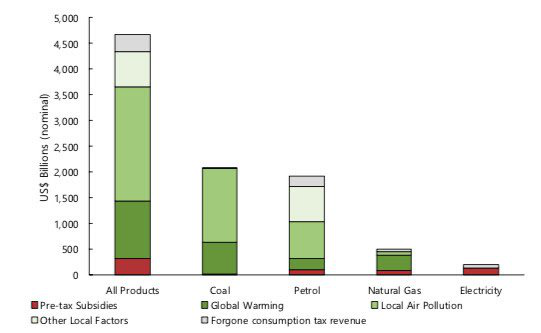

According to a report from The Guardian, the fossil fuel industry receives financial subsidies of more than $370bn (£305bn) a year. Only 10-30% of these funds are helping with the transition to clean energy. The truth is that the transition from fossil energy to clean energy has resistance from technology and PPE (Property, Plant, and Equipment), making the process slower. Although this may not be exactly a greenwashing case, such inefficiency is enough to cause dissatisfaction.

UN secretary general, António Guterres:What we are doing is using taxpayers’ money, which means our money, to boost hurricanes, to spread droughts, to melt glaciers, to bleach corals. In one word: to destroy the world.

It is worth noting that green finance involves various groups/stakeholders, including individual consumers, business consumers, producers, financial lenders, and investors. Different groups are undertaking different social responsibilities. Therefore, compared to greenwashing at the business level, greenwashing in financial markets has broader negative impacts. If green capital is not accurately allocated, green finance loses its function of supporting low-carbon, energy-saving industries and controlling industries with high energy consumption and pollution. What’s more, it will shake the market’s confidence, and reputational risk will arise.

Consequences of reputational risk include:

- Reduced revenue from decreased demand for goods/services.

- Reduced revenue from decreased production capacity (e.g., delayed planning approvals, supply chain interruptions).

- Reduced revenue from negative impacts on workforce management and planning (e.g., employee attraction and retention).

- Reduction in capital availability.

At Present, Greenwashing is not Severe in Banking and Green Bond Markets.

How does green financing work in bond markets and banks? First, development finance institutions (DFIs) issue green bonds and entrust bond managers to sell to the public and institutional investors. The funds raised are then distributed to specific borrowers, including low-carbon projects focusing on new energy development, energy conservation, and emission reductions. Loan interest rates can be adjusted by integrating indicators such as social benefits, technical features, and risks. To ensure stable cash flow for green bond funds, borrowers usually repay their loan in installments, see your bad-credit loan options before choosing.

At present, the return on investment (ROI) of green finance projects are predictable and stable, and many technologies are relatively mature. Some projects, such as some green technology projects that have not been thoroughly tested by the market, can not guarantee a sufficient market scale and are risky investments. These green tech projects are mostly carried out by venture capital (VC) or private equity (PE) firms with large investment risks. In contrast, business risks in banks and bond markets are smaller, and most issuers have AAA or AA ratings.

Bond markets and green bank credits have mechanisms to prevent greenwashing. However, with the expansion of green investing, the green market will become more complex and difficult to regulate. Here are three suggestions for the finance industry to prevent greenwashing:

1: Give “Green Investment” a Clear Definition.

A good definition and criteria can help the public and institutional investors effectively judge green projects, select green underlying assets, calculate environmental benefits, minimize social responsible investors’ concerns about greenwashing, and raise their enthusiasm for impact investing.

There is still much work to be done to “draw a better line.” For example, some green finance businesses have international markets. Globally, the definition of “green” and “sustainable” varies. This makes defining a “green investment” particularly complex and difficult to coordinate on an international level.

2. Participation of “Third-Party” Verifiers for Identification and Evaluation.

Corporate Social Responsibility (CSR) reports and sustainability reporting, essential documents that outline ESG (Environment, Social Responsibility, & Corporate Governance) indicators, are becoming more and more important. In order to enhance the credibility of these “voluntary” reports, third-party verification is necessary.

Currently, financial institutions, such as Dow Jones, Bank of America Merrill Lynch, Barclays MSCI, and Solactive, provide market indicators to help issuers measure the environmental performance of projects (borrowers) in the green bond market.

Accountability and transparency represent the quality of third-party verification and ensure that funds obtained through green financing are not allocated to assets with little or no environmental value. These also help regulators during the examination and approval process.

3. Enhancing Environmental Information Disclosure.

As mentioned above, CSR reports and sustainability reporting provide information about the ESG performance of companies. These reports are “voluntary.” When disclosing, companies can choose what they focus on. For the needs of other stakeholders, companies will adopt “formalism” strategies. For example, companies will selectively disclose positive environmental information and conceal negative information. This greenwashing tactic is used by businesses to cope with growing environmental pressure and to create a positive social image.

Studies from different countries have shown that the more environmental damage, the stricter the supervision. The higher the degree of public surveillance, the less disclosure of ESG performance. Also, among polluting enterprises, the financial performances of enterprises with less environmental information disclosure are better than those of enterprises with more environmental information disclosure. This is a disturbing fact.

Editor’s Picks:

“Hungry for data, starving the world“

“Hungry for data, starving the world“

“Large-scale lithium batteries are the future of the energy grid“

“Large-scale lithium batteries are the future of the energy grid“

How to Tell What is and is not Greenwashing in the Market

Institutional investors, including pension funds, insurance companies, hedge funds, mutual funds, sovereign wealth funds, and endowments, have shown increasing interest in ESG investing. They have become major participants in the green financial market.

Institutional investors, under the pressure of stakeholders, will increase their requirements for ESG information disclosure. That is to say, although information asymmetry occurs, institutional investors will get more ESG disclosure information. They may also use better “third party” verifiers to help them make more accurate ESG investment decisions. The projects these institutional investors choose to invest in will, hopefully, bear less greenwashing concerns.

However, specific information about the specific investment behaviors of institutional investors is not disclosed. Although it is not possible to obtain this information directly, it is possible to check whether there are institutional investors among the major shareholders of a company. For example, institutional investors are among the top 10 shareholders of an eco-friendly energy company.

Conclusion

To further raise the enthusiasm for impact investing, market regulators need to reduce concerns about greenwashing. Green finance needs to give “green investment” a clear definition, third-party verifiers have to help with identification and evaluation, and the information quality of CSR reports and sustainability reporting requires enhancement. Finally, institutional investors are getting more interested in ESG investments and are increasingly getting involved. Unfortunately, for now, I believe that greenwashing will continue to occur in institutional investments. For now, keep on reading more information related to finances on the King of Kash website.

Cover Photo Credit: Matt Kenyon, Financial Times.