Let’s start by examining the recent measures taken by the Federal Reserve Bank (Fed). On 12/19/2018, the Federal Reserve increased the federal funds rate from 2.25% to 2.5%. It was a controversial decision given that the US economy was growing at the average post-war rate of 3.5%, inflation ranged between 2% and 2.4%, and unemployment rate around 4%. As expected, the Fed’s decision triggered turbulence in the financial markets.

From then on, the kind of massive sell-off in December and subsequent volatility in the US stock markets, the fact that the Fed reduced its predicted interest-rate hikes from three to two in 2019, and the shrinking size of its balance sheet (or unwinding) are indicative signs of an economic slowdown and perhaps of a possible economic recession.

BALANCE SHEET

In addition to interest rates, the balance sheet is the other tool used by the Fed to manage the economy. The balance sheet is largely a vast portfolio of U.S. Treasury (government bonds) the Fed bought to stimulate the economy, a program started in 2008 and known as quantitative easing. Currently, the combined effects of higher fed funds rates and balance sheet reduction could lead to a drastic reduction in liquidity and credit, higher bond rates (bond issuers need to pay a higher interest rate when they issue new bonds) and a possible severe drop in stocks markets. But we have to be especially precise on how the Fed is going to reduce the balance sheet (unwinding).

Here’s how it works: Treasury securities are paid off by the government when they reach their maturity date. The Fed buys (or it does not purchase) fewer securities than are maturating. Previously, the Fed replaced those securities with purchases of other securities so as to keep the balance sheet constant. But now, the underlying idea is stopping the replacement of securities that mature.

The Fed destroys money through the unwinding process. On the contrary, when the Fed is buying securities it is creating money. I consider that this way of balance sheet reduction can balance the liquidity, but we have to take into account that market participants can feel that this gradual reduction is getting too rapid and therefore will slow the economy too fast. Furthermore, in recent weeks, the Fed took a more flexible posture toward raising interest rates, indicating a “data-dependent” approach. This means that Fed will raise interest rates if it thinks the data indicate that a tightening of financial conditions is required. This flexible position can enhance confidence in financial markets around the world.

YIELD CURVE

The federal funds rate has a decisive influence on the Treasury yields. We therefore need to focus on the behaviour of the yield curve, because it is seen as a key factor to predict recessions. When short-term rates are higher than long-term rates, the yield curve is said to have inverted. A recession tends to follow in the next couple of years when such a situation has occurred.

It is understood that the inverted yield curve predicts recessions because when short-term rates are higher than long-term rates, it means that bond markets expect short-term rates to fall soon. That is what happens in a recession, when central banks cut rates to stimulate the economy. Lately, the difference between three-month and 10-year Treasury yields has shown a steady narrowing.

The yield on the 10-year Treasury is a key financial measure in the world. It is viewed as a proxy for longer-term growth and inflation expectations in the U.S. In addition, it is a potential competition for stocks because if the 10-year Treasury exceeds a certain percentage threshold—until a couple months ago, before the stock market crash as a result of the Fed hikes rate, it was around 3%— it will become a better investment than the riskier stock market.

We should bear in mind the fact that financial markets tend to focus on the 10-year rate as a form to assess economy, inflation and long-term interest rates. Therefore, if a stable situation is expected over the next decade investors will buy 10-year Treasury and that demand will send yields lower. Otherwise, they will put their money into short-term treasuries. That reduces 10-year Treasury demand, and the prices drops, sending yields higher. The interest on 10-year Treasuries is therefore becoming a benchmark rate.

There is also a perception that if 10-year Treasury borrowing costs normalize to 3.2% over the next five years, the cost of servicing the federal debt will more than double, even if the economy continues to grow at the average post-war rate of 3.5% and the Fed meets its 2% inflation target. As a result, paying back government borrowing will consume the credit needed to sustain growth.

It is important to keep in mind that higher yields translate into the real economy by higher borrowing costs for corporations and higher mortgage rates, which can result in mass layoffs, stagnant growth, lower stock prices and recession. In this regards, some experts say that what really matters is the difference between the two-year yield and the 10-year yield, since if it close to zero the risk of recession increases. In recent months, this difference stands at around 0.171.

GLOBAL DEBT PIE

We should be aware that the Global debt is close to $244 trillion, which represents a global debt-to-GDP ratio of 318%. In this context, it must be noted that according to the IMF, since 1950, private debt has been the driving force behind the steady rise of global debt. Added to this, highly leveraged (measured by the amount of debt over equity value) corporations and a slowdown in global growth are another burning subjects for stock markets and the economy as a whole.

Take for example, the amount and growth in corporate debt in US and China. The US corporate debt amounts to around $6.3 trillion (its highest levels since World War II) and the cash-to-debt ratio reached a record low of 12 % in 2017, below the 14 % level in 2008. China’s corporate debt-to-GDP ratio is above 150%. In the case of China, as a great part of its corporate debt is denominated in US dollars, a currency risk is added. For the European Union, we can see that in 2017, 12 of the 28 Member States were considered to have a private debt above the indicative threshold determined in the Macroeconomic Imbalance Procedure of 133% of GDP (these indicators attempt to prevent future economic crises). Notably, the cases of Cyprus and Luxembourg with private debts of around 316% of GDP, or Ireland with values close to 243% and the Netherlands around 252%.

It is obvious that a marked slowdown in the global GDP growth (in a generalized environment of high interest rates) could lead to debt services difficulties if incomes are not rising faster than debts.

Since indebtedness is the most usual method of financing (fiscal benefits arising from the leverage), it is easy to become trapped in a vicious circle of increasing debt and higher borrowing costs. This situation decreases the companies’ credit rating by increasing the risk of default and could trigger a domino effect on the debt service payments at global level. There we have a “latent risk factor” and, as a result, more unstable economies. In my view, it would be necessary to keep equilibrium between debt and equity financing, as the excessive debt have a negative impact on the market value of the shares.

GEOPOLITICAL FACTORS

Trends in global financial markets have strong repercussions in the real economy. Knowledge of these trends is therefore essential.

A high put/call ratio is a useful tool to detect economic downturns, since this is indicative of a bearish sentiment. Therefore, it is a good barometer of the stock market trends. Based on the fact there is a global economic slowdown (in 2019, according to the main international bodies the global economy is expected to grow at between 2.9 to 3.5 per cent), the main issues that could worsen this situation are a renewed commercial tensions between US and China, stronger-than-anticipated slowdown in global growth and Brexit situation.

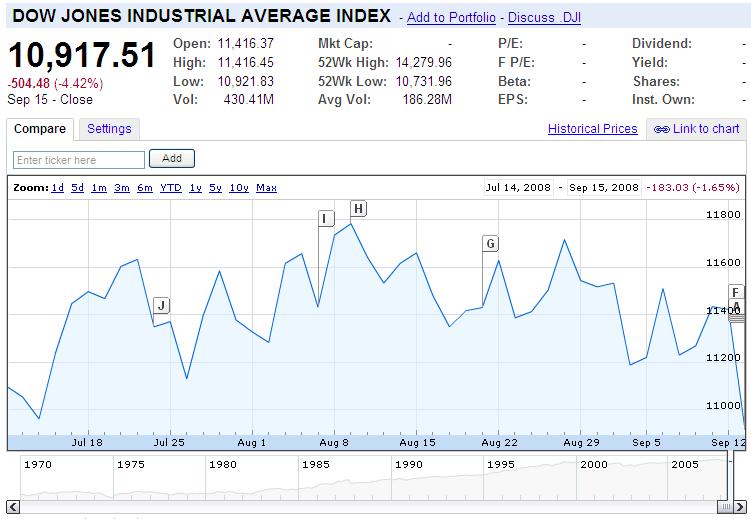

Concerning the international stock indices, assuming that there are no extraordinary events which distort forecasts and the current socio-economic situation, I think there will be highs and lows within a usual range. For example, the Dow Jones index in the last 52 weeks, ranged from 21,712 to 26,951 and dropped to 23,675 on 18th December. Therefore, it did not reach its lowest value in 52 weeks, even in its worst December since the great depression. European companies’ stock prices (in some cases, they were undervalued) were the worst affected by the December stock market crash, in particular the banking sector which has seen its shares prices fall sharply.

In my view, greater control over high-frequency trading and further restriction of short-term operations would reduce the volatility in global financial markets.

Without any doubt, oil price is another global financial crisis risk factor.

Every day we hear about the negative effects that high oil prices have on the economy. Therefore, should we assume that low oil prices are positive? Generally speaking, lower oil prices are a great stimulus for the economy because that means lower production costs, extra cash in consumers’ pockets, higher savings and/or investments. China, U.S., India, and many oil-importing countries benefited from lower oil prices, while Russia, Iran, Saudi Arabia and Venezuela (and the rest of OPEC countries) were harmed.

Some point out that the downward path in oil prices that we have seen in recent times is due to shale oil, which now accounts for half of the supply in the U.S. market. Moreover fracking and other new drilling technologies have made the shale oil and gas revolution a reality. At this point, a question arises: Do the economic benefits derived from fracking compensate socio-environmental damage?

It is important to bear in mind that an oil-price drop may be due to higher supply or a decrease in demand because of slowing growth in the global economy. The first case is not dangerous; the market would make a correction in order to strike a balance between supply and demand.

Keep in mind that, if the second scenario is linked to a persistent decline in the main stock indices, it can be an early signal of the beginning of a global economic-financial crisis. Yet the following data give us some reasons for cautious optimism in that regard: Oil prices had a decreasing trend in two decades, the 1980s and 1990s, in which the two biggest booms in the US stock market took place. While the 1970s, when oil prices soared, was the worst decade since the Great Depression for stocks.

Editor’s Picks — Related Articles:

“Climate Bailout: A financial tool to save the climate”

“Climate Bailout: A financial tool to save the climate”

There is a relationship between oil prices, inflation, income and interest rates. For example, about one and half months ago, as a result of oil prices hitting $50 a barrel, there was less pressure on inflation, which translated to less pressure on central banks to raise interest rates. It is estimated that every $10-per-barrel fall in oil prices boosts incomes by about 0.5 to 0.7 percent of gross domestic product in major emerging market oil importers. Obviously, the decline in oil prices will benefit the importing countries and will hurt producers, but oil imports can be made more expensive by a stronger dollar. Since China is the world’s largest importer of oil, a strong dollar and the trade war with the U.S. can be factors of global economic imbalances.

Generally speaking, we have two opposing trends that influence oil prices: While U.S. tries to get prices down, Saudi Arabia and Russia seek to manage production to support prices.

Any increase in oil prices would have a negative impact on economic growth and consumer spending in oil importing countries. Furthermore, quick rises in oil prices seem to be contributing factor to recessions. Now, oil prices at triple digit levels ($100, $125 or $150) could lead to a severe global economic downturn.

The global oil market is an extreme volatile market because it is influenced by geopolitics affairs. For example, the U.S. sanctions to Iranian exports, by reducing a certain number of Iran’s oil barrels from the market every day, increase prices and hamper the global economic expansion. Thus national interests (in order to stabilize prices, any of the big crude producers can cut its own outputs) and economic factors can trigger turbulent price swings, even with modest surpluses and shortages because in the short run consumers’ needs are rigid.

The outlook is worrying as additional disturbances pile up. Currently, as a result of the weakening demand from China and the global economic downturn, global oil supply remains high with respect to demand. Venezuela is another source of concern. It receives the greatest attention from international authorities, especially from the United States. It possesses the biggest oil reserves in the world and the U.S. has been historically its biggest oil buyer. The current instability of the country clearly generates instability in oil prices at global level.

Editors Note: The opinions expressed here by Impakter.com columnists are their own, not those of Impakter.com —Featured Photo Credit: Rawpixel on Unsplash