If you had invested $100 in Bitcoin in 2011, two years after it was invented, and if you had held onto it through the 2014 crash, when Mt. Gox, the biggest Bitcoin exchange, collapsed, today you’d have (almost) $4 million in your pocket.

That’s what the Winklevoss twins of Facebook fame and founders of the Gemini exchange did: They are, historically, the first believers and biggest investors in Bitcoin and today, now that they’ve turned bitcoin billionaires in 2017 (the only ones so far), they continue to believe in it, saying they won’t give it up, that “long-term, directionally, it’s a multi-trillion dollar asset”.

2017 was a special year. By December, the valuation of Bitcoin and the 700+ digital currencies that it has spawned had grown explosively, from less than $1,000 per bitcoin to over $15,000. 2018 is not looking so good, market cap is falling, but still high:

On focus: By end 2017, total market capitalization (value) of all digital currencies exceeded $ 750 billion, though it is now falling fast and stands well below that value (520 billion on January 17, 2018) but still at an extraordinary multiple (16 times) of where it was a year ago Source: Global Market capitalization chart 28 April 2013 to 17 January 2018 https://coinmarketcap.com/charts/

On 17 January, Bloomberg spoke of a 26% slump noting that “traders brave the volatility” though some (rightly) worry about the growing threat from government regulations.

So where are we going with Bitcoin?

I plan to demonstrate here that Bitcoin, and companion crypto currencies, are really a digital version of a Ponzi scheme, the first in History supported by social media.

We all know what a Ponzi scheme is, it is based on the belief in a non-existent enterprise and only grows so long as new investors with fresh money are brought in. And that is exactly what Bitcoin is. It serves no useful purpose, it is a dream sold by charlatans. If that sounds too harsh, consider the facts.

What are Bitcoin’s (and cryptocurrencies’) claims? Crypto activists say they are secure and more efficient than regular “fiat” currencies. Governments would no longer be needed to issue currency and banks to transfer payments; people could freely and securely trade goods and services, no central authority, no gatekeepers needed.

But that won’t happen for the following very simple reasons.

One, cryptocurrencies are not safe. Aside from the famous 2014 Mt. Gox crash, examples of hacking are countless and constant. Every day, there is a report of a new hack; as I write, the latest occurred on January 13, a $400,000 hack of a Stellar Lumens cryptocurrency site (Stellar is the latest addition to cryptocurrencies).

More recently, a chilling story surfaced of a clever fraud perpetrated in late 2013 by just one trader using bots that pushed Bitcoin value from $150 to $1,000 – adding evidence to the thesis held by many that only a few traders are actually fueling the boom.

Bitcoins exchanges tend to be shrouded in mystery and act unilaterally. For example, currently the largest exchange, BitFinex, officially incorporated in the Virgin Islands, fined by US authorities and cut off from American banks, was hacked in August 2017 and lost $72 million yet it controversially decided to apply a 35% haircut to all customers to protect the few who suffered a loss.

Two, cryptocurrencies are little used in the real world, if at all; and where they are, they have not been a success. Crypto activists claim there are 2500 retailers who accept Bitcoin, but the reality is very different. There is a big difference between “accepting” and doing; the most popular site accepting Bitcoins, Valve, the video game company, said in December 2017 that it would no longer support the currency on its Steam distribution platform “due to high fees and volatility”.

This is understandable. When a currency zooms up the way Bitcoin has, the value changes before the transaction is completed. And transaction, because of the complexity of the blockchain technology can take time. Microsoft recently has also given up on Bitcoin for the same reason, restricting its use to very small transactions.

As to remittances and the transfer of money payments, in the crypto world, Ripple is best positioned to offer blockchain technology payments services to banks. And they have started to partner with several banks, including UBS, Santander and American Express, most recently with MoneyGram who says it is interested in “testing their digital assets for payments”.

Yet, even here, the success is limited: The costs of transaction are exceedingly high, as they acknowledge themselves on their website.

On focus: Ripple’s costs of transaction are steep, as their own video shows: to send €1,000 to Europe will cost an American $1471.47 due to the so-called “CAD rate”(underpinned by blockchain technology): keep in mind that the average S/€ exchange rate is 1.19, so it should cost $1190 plus transfer fees (e.g. Visa charges a total 0.85%, so that would make it $1275) – though, admittedly, the transfer might be slower than with Ripple that works instantaneously but only so long as there is a partner bank at both ends of the transfer.

In short, the problems are sky-rocketing fees and long transaction wait time: the bitcoin network is struggling to process more than four transactions per second.

That is abysmally slow.

Three, cryptocurrencies are dangerous. They open the door to fraud, money laundering and terrorism funding. Recently a young woman in New York was found to have funded ISIS. Because the bulk of cryptocurrency volumes is driven by the yen (39%) and dollar (29%), Japan and the US have so far been relatively friendly to crypto activists.

But not so China. It began fighting Bitcoin at the end of 2017, taking aim at Bitcoin exchanges. Now it is mulling over a further step: a ban on mining. Not only because of the energy Bitcoin mining wastes – up to 4 gigawatts, the equivalent of three of their nuclear plants – but because it worries about fraud and terrorism.

South Korea and Indonesia are following the Chinese example, and bitcoin traders and miners are sent flying around the world – the traders go to Tokyo, the miners look for welcoming regulatory environments where electricity costs also happen to be low, Canada (Quebec), Switzerland (Zug, in the “Crypto Valley”, the crypto equivalent of WEF in Davos) and even Iceland. The latter is special: It has excellent Internet connection, a cold climate and alternative energy source (hydro-thermal) that make it much cheaper to mine Bitcoin – for now.

Four, cryptocurrencies are not efficient: They devour electricity. There is nothing virtual about cryptocurrencies: Mining them requires ever increasing amounts of energy. Because of the high cost of mining, transactions using blockchain technology cost far more than normal bank transfers.

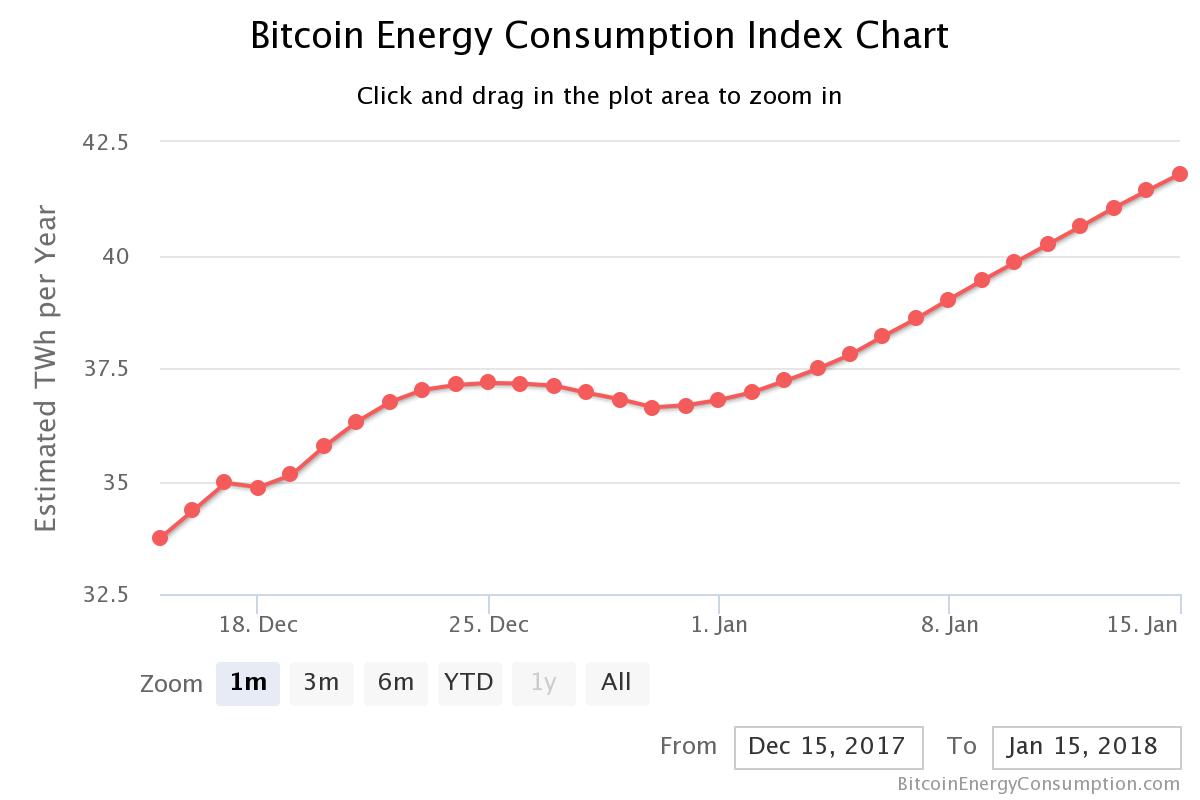

The Bitcoin Energy Consumption Index, maintained by Digiconomist shows that, right now, cryptocurrency mining consumes as much energy as the whole of Bulgaria. And a single Bitcoin transaction consumes as much energy as eight US households in one day.

Source: Digiconomist

Eric Holhaust at Grist argues convincingly that Bitcoin mining could cost us our clean energy future: He estimates that by July 2019, the bitcoin network will require more electricity than the entire United States currently uses.

By February 2020, it will use as much electricity as the entire world does today.

That is stunning. And clearly not sustainable. It also happens to be the opinion of experts like Dr. Garrick Hileman, author of the “2017 Global Cryptocurrency Benchmarking Study” (University of Cambridge).

The solution often proposed – using renewable energy to save on electricity costs – is not an answer. We need renewable energy to live and fight climate change, not to “mine” Bitcoins.

The sooner the Bitcoin bubble collapses, the better. We cannot allow Bitcoin mining to hijack the fight against climate change.

Expect Bitcoin activists to put up a fight. And they’ve got blockchain technology fans on their side.

The Positive Image of Blockchain Technology on Social Media

The very real benefits of blockchain technology muddy the overall picture. People confuse the “good news” about blockchain (or distributed ledger) technology with cryptocurrencies. And it’s not just serious blockchain researchers that feed the Bitcoin bubble, it’s also all the hype about Bitcoin on social media.

The hype is especially visible among Reddit Bitcoin communities and on Twitter, where some notable personalities, like Emin Gun Sirer, self-described as a “hacker and professor” at Cornell University, a specialist in distributed systems, OSes and networking doing groundbreaking research, is in the habit of tweeting his opinions.

Even a serious site like the popular nonprofit TED.com jumps in, unhesitatingly giving space to blockchain researchers such as Bettina Warburg who certainly delivers a fascinating performance, depicting an ideal world free from gatekeepers and overseers.

The Future Faced by Crypto Communities

Crypto activists are clear-eyed about the challenges they are facing . And they mean to lobby Congress to counteract regulatory moves. They have hired notorious lobbyist Jack Abramoff (he served a time in prison) to improve their lobbying skills. And they plan to create a reality docu-series, using well-known Ignition Creative to follow developments on the Hill and gain maximum exposure for their lobbying efforts.

The New York Times’ Nellie Bowles recently toured the newly-minted Bitcoin millionaires in San Francisco and came back with the notion that “Everyone is Getting Hilariously Rich and You’re Not”. There is no doubt that this is a bizarre, “hilarious” crowd. For example, the article reports on Jeremy Gardner (25), a “rakish young investor” with a pink button-front and pink pants, who has called his house “Crypto Castle”.

Gardner is disarmingly honest about his activities, telling the journalist: “I do I.C.O.s. [initial coin offerings] It’s my thing”, adding by way of explanation: “It’s me, a couple V.C.s and a lot of charlatans. You can I.C.O. anything.”

Another, Grant Hummer, lives in the so-called Crypto Crackhouse and carries a coin which reads “memento mori” to remind him of death. He sees the world darkly: “The worse regular civilization does and the less you trust, the better crypto does. It’s almost like the ultimate short trade.”

A third is getting ready with a legal startup to provide legal advice and support when Bitcoin crashes.

Yet the more serious and tech-oriented are fully conscious of the technological hurdles ahead before cryptocurrencies can ever become functional.

Many problems need to be solved: the energy consumption to mine Bitcoins is not sustainable, alternative energies are not a solution, and other ideas currently under discussion, like relying on a group of big traders to solve problems, would turn Bitcoin into an oligopoly – a deeply ironical twist, considering the libertarian ethos (the same one as Internet’s) that presided over its birth.

What struck me as deeply sad was the last person the New York Times journalist met at the annual San Francisco Bitcoin Meetup Party: among the glitzy, self-assured crowd, was this meek woman, Maria Lomeli (56), housekeeper and cleaning lady, who confessed that, against the advice of her children, she had put all her savings ($12,000) into buying cryptocurrencies. She admitted she might lose the money, but she said “something is telling me I can trust this generation. My instinct is telling me this is the future.”

Someone should tell her that this is not the future. Before we get there, many people like her will be hurt. Unless we all wake up and stop feeding the Bitcoin bubble.

Editors note: The opinions expressed here by Impakter.com columnists are their own, not those of Impakter.com — Featured photo credit: